A quarterly update on the building decarbonization movement

Q1 | 2026

Authors

Kristin George Bagdanov, PhD, Associate Director of Research

Kevin Carbonnier, PhD, Associate Director of Analytics

About Our Research

BDC tracks and analyzes policies, trends, and data to accelerate the building decarbonization movement. We synthesize qualitative and quantitative data to produce rigorously researched, substantively contextualized, equitably cited, and endlessly shareable resources that help move our movement forward. We believe that research only becomes knowledge when it’s shared, so please pass along these resources to your communities and help us equitably decarbonize our buildings and neighborhoods. Read more about our research philosophy, resources, and reports.

Table of Contents

I. The Big Picture

II. Market Momentum

III. Neighborhood Scale

IV. Gas System Costs and Affordability

V. The Thermal Transition

VI. Looking Ahead

VII. Methodology

I. The Big Picture

What happened this quarter in the building decarbonization movement

From the ever-expanding energy demand of data centers and AI-driven campaigns to weaken appliance standards, to the growing list of repealed regulations intended to protect public health and the environment, 2026 looks different from the future many of us envisioned when we began working on building decarbonization.

Progress, however, is rarely linear. While some areas appear to be regressing, others reveal surprising innovation, momentum, and durability across the United States.

Federally funded home energy rebates, for example, remain active in a dozen states and the District of Columbia (tracked by the Atlas Building Hub). A national consensus is forming around the importance of energy affordability. States are reforming rate structures, scrutinizing unnecessary capital expenditures by utilities, and—in the case of New Jersey—even freezing rates temporarily.

This report cuts through the noise to highlight those lasting shifts: the proceedings, legislation, protections, and investments that signal steady, if uneven, progress in the unfolding thermal transition.

Read on for the full report and download the executive summary below.

Overview

Here are major events and actions shaping building decarbonization in the first quarter of 2026:

Market momentum

- Heat pumps outsold gas furnaces for the fourth year in a row.

- Heat pumps outsold air conditioners for the first time ever.

- The shift to clean heat is already reshaping America’s 4.5 million-strong heating and cooling workforce.

Gas system costs and affordability

- Gas utility spending on distribution infrastructure has more than tripled since 2010, and customers would have saved $130 billion ($1,723 per gas household) if utilities had maintained pre-2010 levels of investment instead of dramatically accelerating spending.

- Each year of accelerated gas utility spending adds at least $40 billion in excess lifetime costs for ratepayers.

- About two-thirds of a typical household’s gas bill now goes to delivery and infrastructure, rather than the gas itself.

- In 2025, gas bills rose 60% faster than electric bills, and four times faster than the rate of inflation.

- One in four households reported forgoing food or medicine to pay for energy bills in 2024.

Utility regulation and the shift away from gas expansion

- States are beginning to unwind financial incentives for new gas expansion by eliminating gas line extension subsidies.

- Non-pipeline alternatives (NPAs) are now shaping pipeline investment decisions across multiple states.

- CKenergy Cooperative (OK) shows utility-led geothermal can improve system economics and affordability at scale.

State action to scale equitable electrification

- California launches its first IOU-scale tariff-on-bill electrification pilot to reduce upfront cost barriers to home electrification.

- California identified 151 priority zones for up to 30 neighborhood-scale decarbonization pilots.

- Building on its seasonal heat pump rate, Massachusetts is emerging as a national leader in utility rate reform: tying bill discounts to household energy burden while creating a regulated pathway to scale thermal energy networks.

- New York locks in long-term funding to scale building electrification—including low- and moderate-income programs—through 2030.

Demonstrating the durability of decarbonization

Equipment Sales

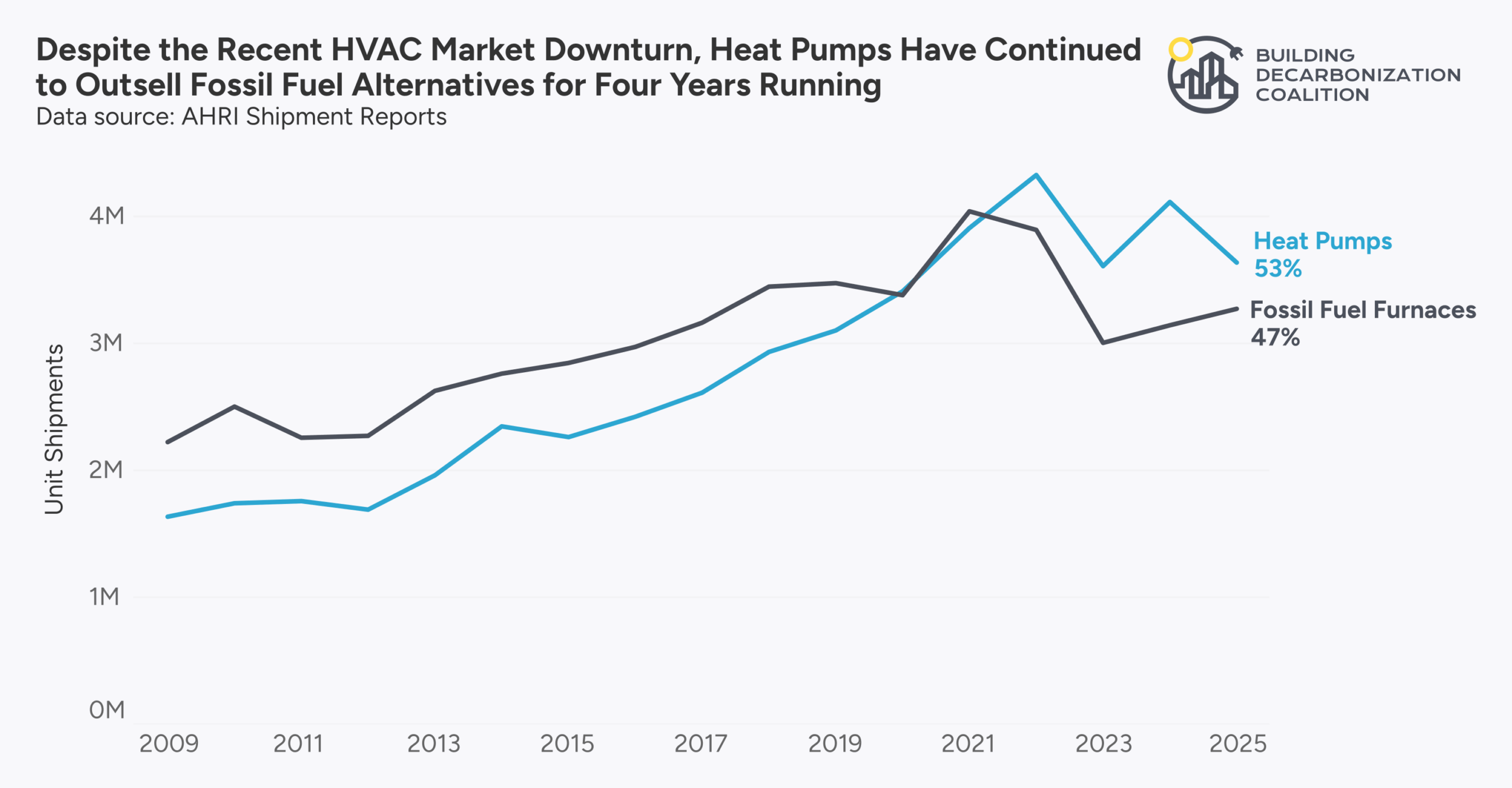

Figure 1: Heat pump and fossil fuel furnace shipment trend

2025 was a slow year for the HVAC market overall. Tariffs, the refrigerant transition, and affordability concerns all contributed to lower equipment sales, especially for air conditioners. Even amid that slowdown, heat pumps outsold fossil fuel furnaces for the fourth year in a row, another sign that the shift toward clean and efficient electric heating is proving durable.

In new construction, the market continues to move even faster. For example, in California, builders are increasingly choosing all-electric homes, avoiding gas service line and connection costs while pairing new buildings with highly efficient heat pumps. Heat pumps are 3-5 times more efficient than gas appliances, making them an important driver of long-term building decarbonization.

We expect heat pumps to continue gaining market share, driven by all-electric new construction, stronger economics from incentives and emerging heat pump rate designs, and consumer interest in replacing aging HVAC systems with equipment that can both heat and cool.

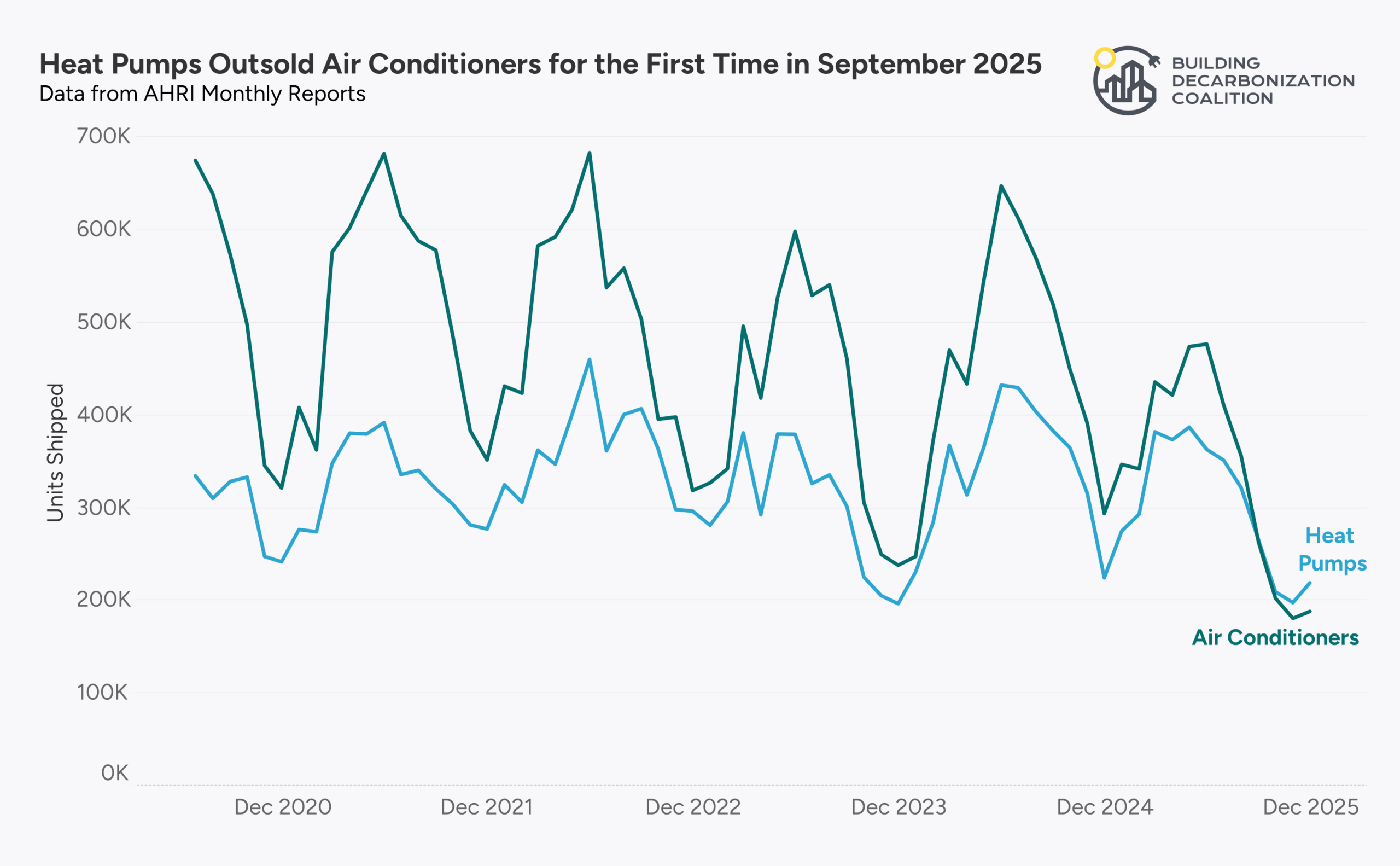

Figure 2: Heat pump and air conditioner shipment trend

A second milestone emerged in late 2025. Although air conditioner sales typically fall in the winter, monthly air conditioner sales dropped below heat pump sales in September 2025 for the first time. That crossover may not hold through the summer, when air conditioner demand peaks, but it is still a notable marker of the market’s direction. Over the last decade, equipment sales have steadily shifted away from one-way air conditioners toward two-way heat pumps that provide both heating and cooling. If that trajectory continues, annual heat pump sales could surpass annual air conditioner sales within the next few years.

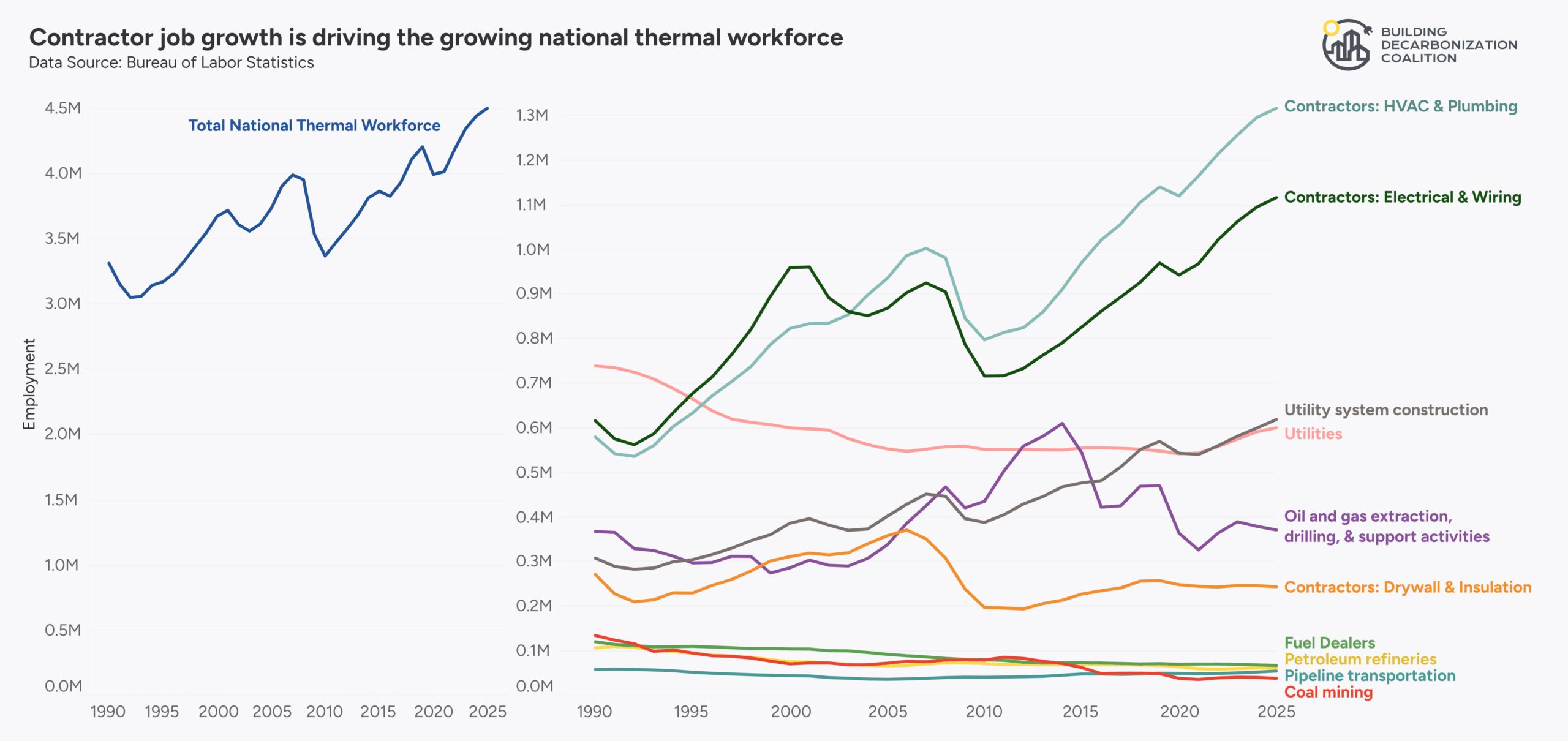

As states translate climate commitments into heat regulation, financing, and market mandates, the success of the thermal transition increasingly hinges on workforce capacity. A managed gas transition requires a diverse and skilled labor force. We use the term thermal workforce to describe the full spectrum of workers who deliver heating and cooling to buildings across fossil fuel and clean energy systems, rather than dividing this workforce into “fossil fuel” and “clean energy” categories.

This framework recenters decarbonization around the delivery of thermal services instead of the fuels behind them, aligning workforce planning with how heating systems actually evolve over time. Rather than treating clean energy and fossil fuel jobs as exclusive or opposing, the thermal workforce framework recognizes these ends of the energy spectrum as part of a continuum focused on providing reliable, affordable, and increasingly clean thermal service.

The thermal workforce includes gas utility workers, pipeline and utility construction crews, and drillers, alongside electricians, plumbers, HVAC technicians, insulators, and other building energy professionals. It spans union and non-union labor, large utilities and small contractors, and urban and rural communities. Importantly, it reflects the reality that the transition from fossil fuel heat to clean heat will occur over decades and will require workers who can operate across systems during the transition period.

The chart below illustrates the workforce segments most directly implicated in the shift from fossil heating to electrification and thermal energy networks.

Figure 3: (Left) Total thermal workforce employment. (Right) Thermal workforce by category.

Altogether, these occupations represent approximately 4.5 million workers nationwide, a workforce that has steadily grown over the past two decades. Collectively, this diverse workforce represents a deep pool of skilled workers who are capable of delivering safe and efficient heating and cooling under evolving technologies and policy frameworks.

The scale and alignment of this workforce also carry direct affordability implications. Labor shortages or skill mismatches can slow electrification projects and increase installation costs, particularly as demand accelerates. Workforce planning is therefore a core affordability and implementation strategy in the thermal transition. As regulatory reform accelerates, workforce planning is moving from a peripheral workforce development issue to a central pillar of building a durable future of clean heat.

Supporting the Thermal Workforce in Colorado

A recurring barrier to heat pump deployment is not necessarily demand but contractor availability and capacity. In January 2026, Power Ahead Colorado (an ambitious program led by the Denver Regional Council of Governments to reduce the environmental impact of the region’s building sector) and the Building Decarbonization Coalition launched the Colorado Contractor Hub, a free, centralized digital workspace designed to help Colorado heat pump contractors grow their businesses and accelerate adoption.

Built around contractor needs, the Hub bundles customer leads, training (with reimbursement for training costs), a one-stop guide to rebates/incentives and permitting, a technical resource library, and a curated marketplace of third-party tools—plus an AI assistant to answer questions on incentives, codes, licensing, and program requirements. It also offers a free Small Business Scaling Program to support companies expanding into electrification and weatherization.

Scaling up building decarbonization, block by block

Our neighborhood-scale project map tracks projects across North America, ranging from fully decarbonized neighborhoods to early plans to transition from fossil fuels. This crowdsourced map is constantly being updated with new projects and we need your help to keep it current. Please submit neighborhood-scale projects for consideration here.

Not included: It does not include all-electric neighborhoods that did not transition away from fossil fuels, or that are within communities with zero-emissions building standards. To learn where local and state governments are encouraging and requiring all-electric buildings, please visit our Zero Emissions Building Ordinance Tracker!

This map shows growing momentum to decarbonize existing neighborhoods by transitioning them from aging gas infrastructure to clean energy infrastructure.

See our full Neighborhood Scale Map on our webpage for additional information and functionality.

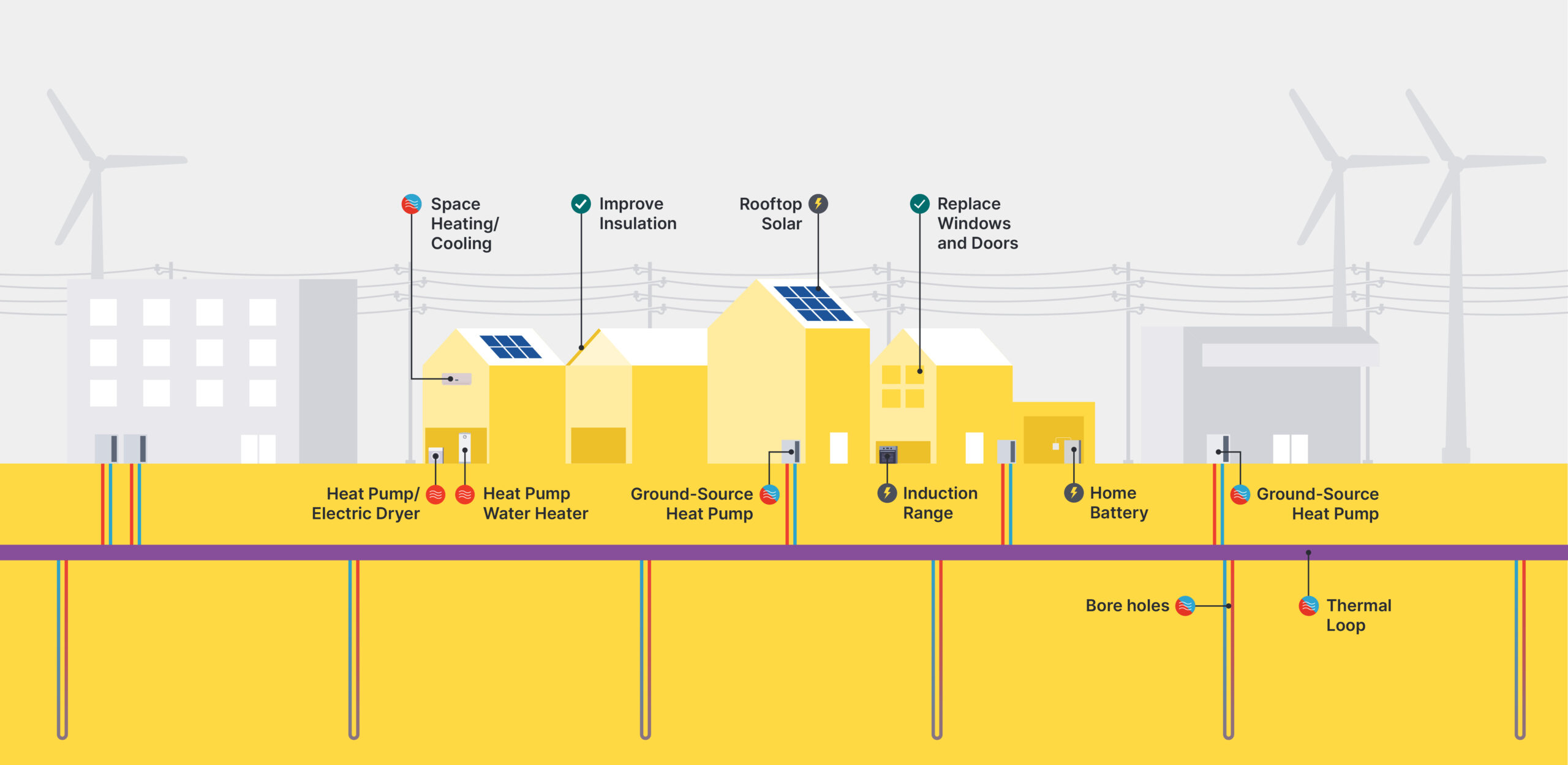

How to Finance a Thermal Energy Network

Thermal energy networks (TENs) are long-lived, infrastructure-scale projects, so financing is less about finding one pot of money and more about matching the right tool to the right project phase and asset. Early dollars tend to support feasibility, community engagement, and design; long-term dollars (like bonds) tend to pay for long-lived assets like borefields and distribution piping; and ongoing revenue tools (like tariffs or service contracts) keep operations stable and affordable over time.

A practical financing roadmap (from concept to operations) includes:

- Feasibility to Pre-development: grants, public programs, technical assistance, and philanthropy to do the scoping, engineering, and engagement work.

- Capital stack and ownership: combine tools (often bonds/green banks + SRFs + grants, sometimes TIF), then pick the ownership/governance model that determines what funding is available (public, PPP, cooperative, etc.).

- Build and operate: finance by component (thermal resource, network, energy center, customer connections), then recover costs through on-bill tariffs, service contracts, or revolving repayment with ongoing community accountability.

To learn more, read our full report here.

Illustration of a thermal energy network

Project Highlight: CKenergy Cooperative, OK

CKenergy Cooperative in western Oklahoma offers a powerful proof point for utilities interested in TENs: namely, that even without a shared thermal network (its territory is too rural for connected piping), utility-led geothermal heat pump deployment can improve system economics and affordability at scale. By helping install ~1,650 geothermal heat pumps across a co-op serving ~27,000 customers (18,000 of which are residential), CKenergy reduced peak demand, improved load factor, and lowered wholesale power costs: benefits that flow to all members, not just the households that adopt geothermal.

- ~27,000 customer meters served (≈18,000 residential)

- ~1,650 geothermal heat pump systems installed (homes, schools, and commercial buildings)

- Member-funded “rider” model covered early incentives: roughly $4–$5/month for a typical household (temporary, not permanent)

- Incentives + financing helped overcome upfront costs: about $3,625/ton in rebates; optional loans up to $15,000 at 6% (4–7 years)

- Program became self-sustaining after ~12 years as reduced wholesale power purchases replaced the need for the rider

- Affordability outcome: “We haven’t had a rate increase in eight years, and we are years away from one now,” said Boyd Lee, retired VP of Strategic Planning, CKenergy and founder of Outside the Box Geo

To learn more, read our full case study.

IV. Gas System Costs and Affordability

How gas system spending is driving energy costs

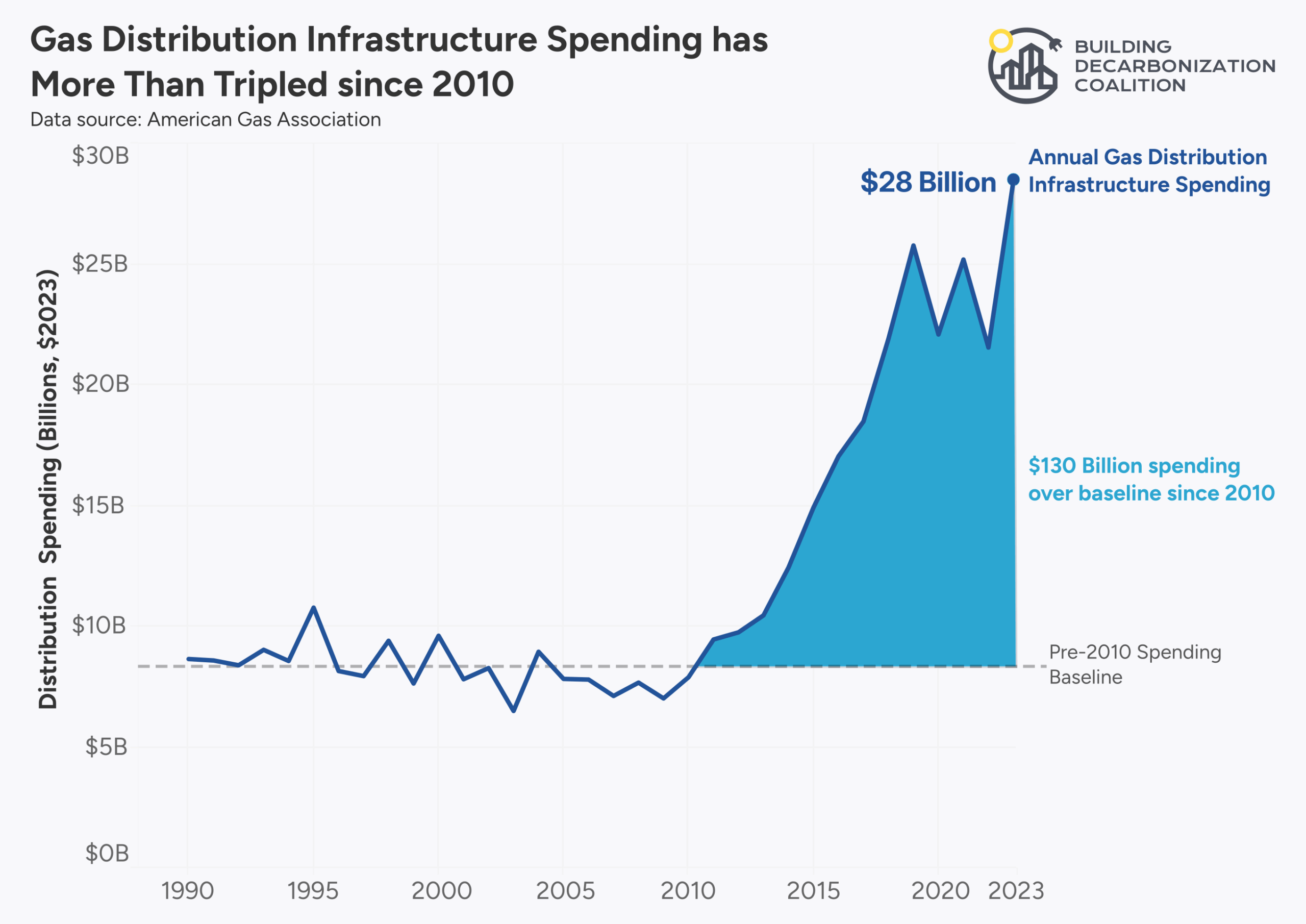

The U.S. gas system is increasingly expensive, aging, and inefficient—and over the last decade, gas utility spending has shifted from business-as-usual investment to an era of accelerated capital expansion.

Gas utility spending on distribution infrastructure has more than tripled since 2010. If utilities had continued the pre-2010 pace of investment instead of dramatically accelerating spending, customers would have saved an estimated $130 billion, or $1,723 per household with gas in the U.S.

Figure 4: National Gas Utility Spending on Distribution Infrastructure

Because every dollar of direct capital spending translates into $2 to $3 in ratepayer costs over the life of the asset due to financing costs and shareholder returns (Synapse), each additional year of accelerated spending creates at least $40 billion in excess lifetime costs.

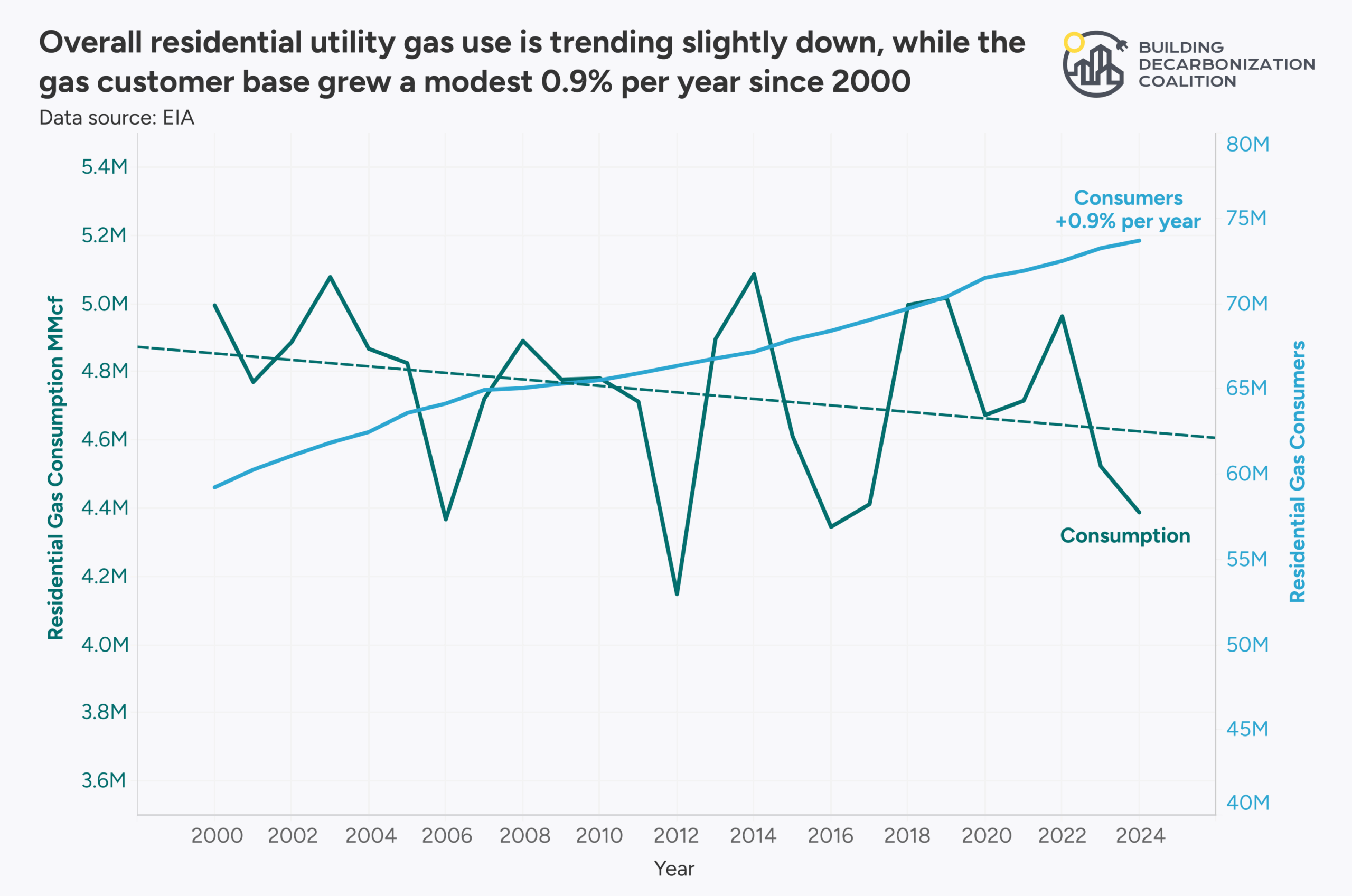

At the same time, gas use is not keeping pace with spending. Over the past decade, residential gas consumption was flat, while the number of residential customers grew only 8.5% (EIA 1, 2). The result is a top-heavy gas delivery system: an expanding asset base with accelerating capital costs that must be recovered from a relatively stagnant pool of customers. In fact, according to the American Gas Association (AGA), the share of infrastructure (and its related costs) per customer has roughly doubled over the last decade (AGA, “Gas plant per customer”). In other words, as customers are utilizing the gas system less, gas utilities are investing—and charging customers—more.

Figure 5: Residential gas customer and consumption trend

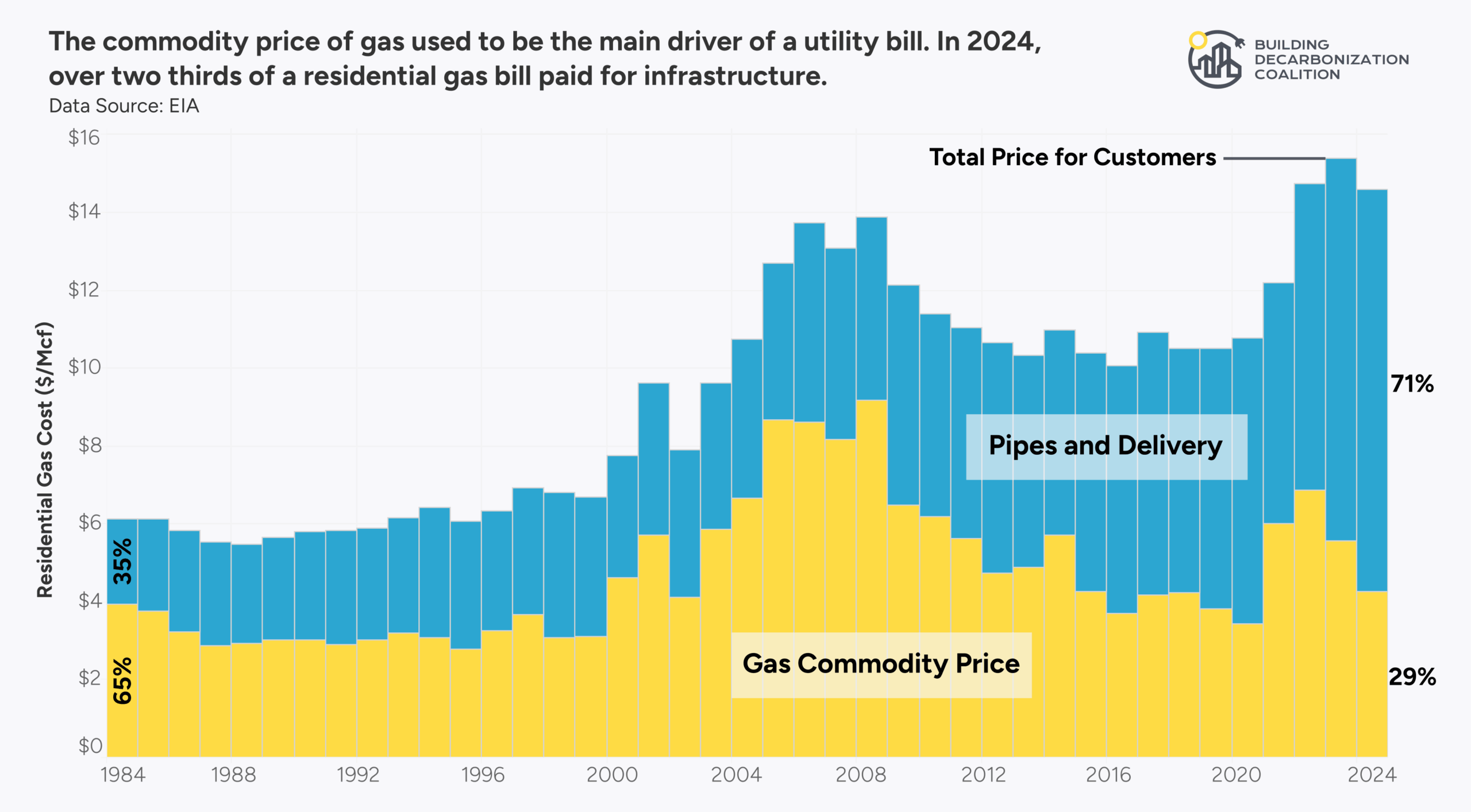

Meanwhile, a growing share of customer bills is paying for the system itself rather than the gas customers actually use. In 2024, about two-thirds of a typical household’s monthly gas bill paid for infrastructure and delivery, while only one-third paid for the fuel (NPR; US EIA citygate, residential data). While some delivery charges vary with usage, a significant portion consists of fixed charges, meaning that even if a customer used no gas, these charges would still appear on the monthly bill.

Figure 6: National gas utility bill composition

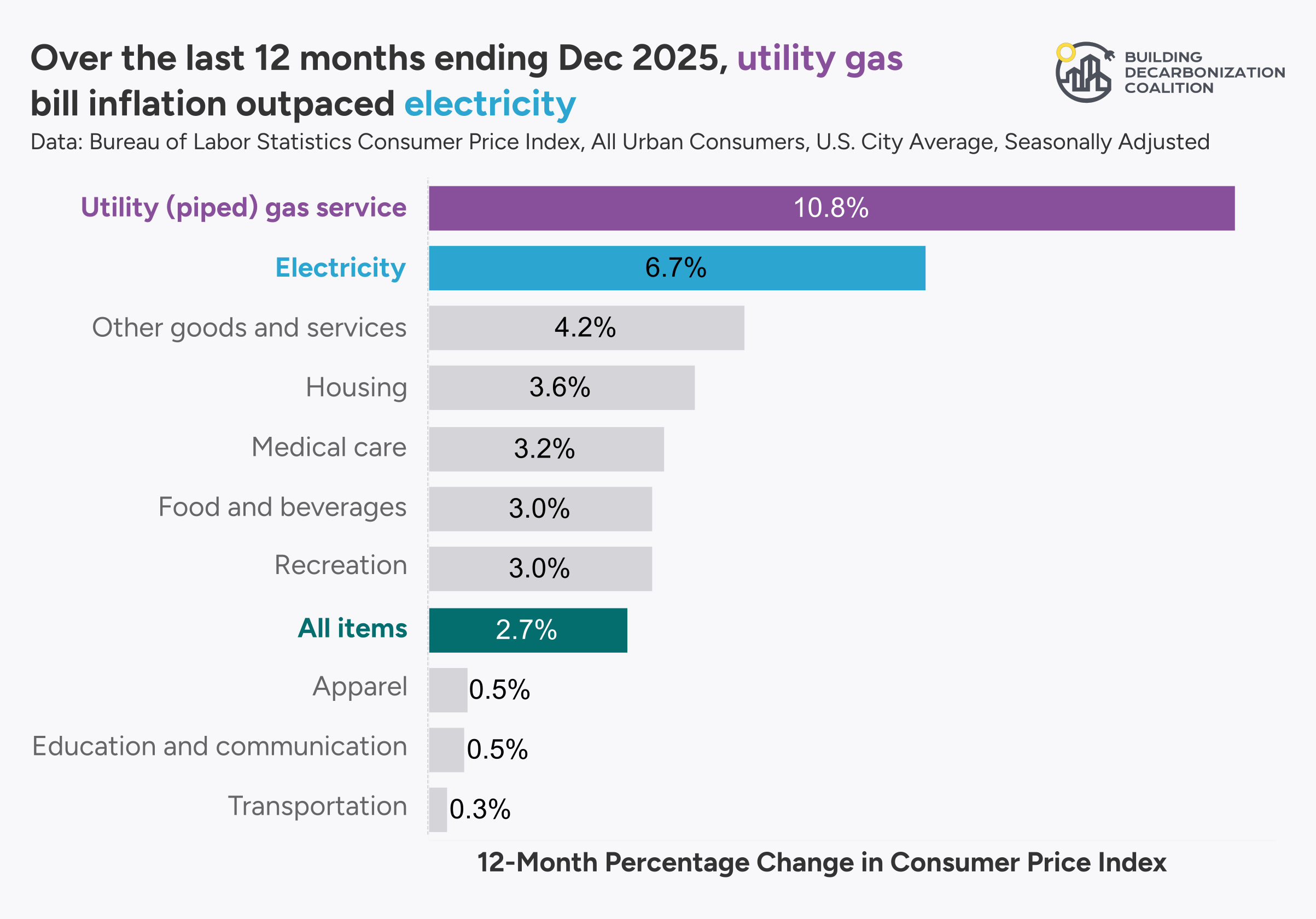

In 2025, gas bills rose 60% faster than electric bills and four times faster than inflation (BLS). That same year, gas utilities requested $3.83 billion in rate increases, reflecting continued investment, especially in pipeline replacement programs (S&P Global). Meanwhile, newly released data from the 2024 RECS survey, show that one-third of households experienced some form of energy insecurity, with one in four households needing to reduce or forgo food or medicine to pay their energy bills. In addition, a 2025 Consumer Reports survey found that 68% of households said their finances were strained to some degree by electricity and gas bills, while 23% said they were very strained (Consumer Reports).

Figure 7: Consumer price index change, Dec 2024 to Dec 2025

Because nearly every end-use in homes and businesses can be served by electricity, there is little justification for continuing to expand and over-invest in two parallel energy delivery systems, especially when one is already showing signs of declining utilization and rising per-customer costs. This period of accelerated gas spending now represents a critical point of intervention: decisions made today will determine whether ratepayers continue funding expensive gas assets that are used less and less, or whether these investments begin to shift toward strengthening and modernizing the electric grid that every building ultimately depends on.

From fossil fuels to clean thermal infrastructure

The thermal transition is the long-term evolution of the thermal sector toward cleaner, more affordable, and more efficient ways of delivering heating and cooling. It offers an inclusive framework for understanding the future of heat: a shift away from the legacy fuels and systems that once defined the heating industry and toward modern solutions that support cleaner air, healthier communities, and lower energy bills.

In this section, we track the legislation and regulatory proceedings helping manage the transition from the gas system to clean thermal infrastructure, including electrification and thermal energy networks.

2026 Legislation

A sample of bills that are enabling the thermal transition

|

State / Bill |

Description |

Categories |

|

California, Industrial Heat and Jobs Act (AB 2088) 🟡 In Progress |

Enables gas utilities to serve customers with a thermal energy network. Also requires the CPUC to initiate a proceeding to establish a regulatory framework for TENs. |

Thermal energy networks, obligation to serve |

|

California, Residential Heat Pump Systems (SB 222) 🟡 In Progress |

Standardizes the heat pump permitting process by creating a pathway for automated permitting, caps permit fees, and establishes guardrails on setback and noise limits. |

Permitting, electrification |

|

Illinois, Gas Appliance Labeling (HB4272) 🟡 In Progress |

Requires a warning label on natural gas appliances that are manufactured on or after January 1, 2027 |

Labeling, consumer protections |

|

Illinois, POWER Act (SB4016/HB5513) 🟡 In Progress |

Establishes consumer protections that minimize the impact of data centers on utility bills and water usage. Also requires data centers to pay into a Public Benefits and Affordability Fund |

Data centers, consumer protections |

|

Indiana, Electric Utility Affordability (HB1002) 🟡 In Progress |

Establishes performance-based ratemaking, requires electric utilities to provide assistance to low-income qualified households, and creates a summer disconnection moratorium for low-income qualified households. |

Affordability, rate reform, consumer protections |

|

Maryland, Maryland Strategic Energy Investment Fund – Required Uses – Building Electrification and Transportation Electrification (SB622) 🟡 In Progress |

Requires the use of the Maryland Strategic Energy Investment Fund for providing loans and grants for building electrification. |

Funding, building electrification |

|

Minnesota, Utility Thermal Energy Network and Jobs Act (SF4281) 🟡 In Progress |

Authorizes regulated gas and electric utilities to implement and cost recover TENs beyond pilots, extends gas consumer protections to TENs customers, and sets priority zones for TENs siting including environmental justice communities. |

Neighborhood-scale thermal energy networks, obligation to serve |

|

New York, Pipelines Leaks & Safety Act (A10071/S9075) 🟡 In Progress |

Requires gas utilities to produce publicly accessible maps indicating planned work on aging pipeline infrastructure and directs the public service commission to designate neighborhood priority decarbonization zones. |

Gas system planning |

|

Washington, Authorizing Community Scaled Weatherization Projects (HB2338) 🟡 In Progress |

Expands what projects can be funded by state programs to include improvements such as energy efficiency, weatherization upgrades, and structural repairs. This allows building condition and energy performance to be addressed at the same time. |

Energy efficiency, funding |

Future of Gas

The “Future of Gas” is an evolving policy framework used to describe the questions, assumptions, and arguments surrounding the long-term sustainability of the methane gas system. Researchers, state energy offices, legislators, and utility regulators have used the phrase to describe policies, reports, and proceedings since at least 2019. Advocates have also applied it retroactively to highlight the growing number of regulators and legislators critically examining the gas system’s longevity.

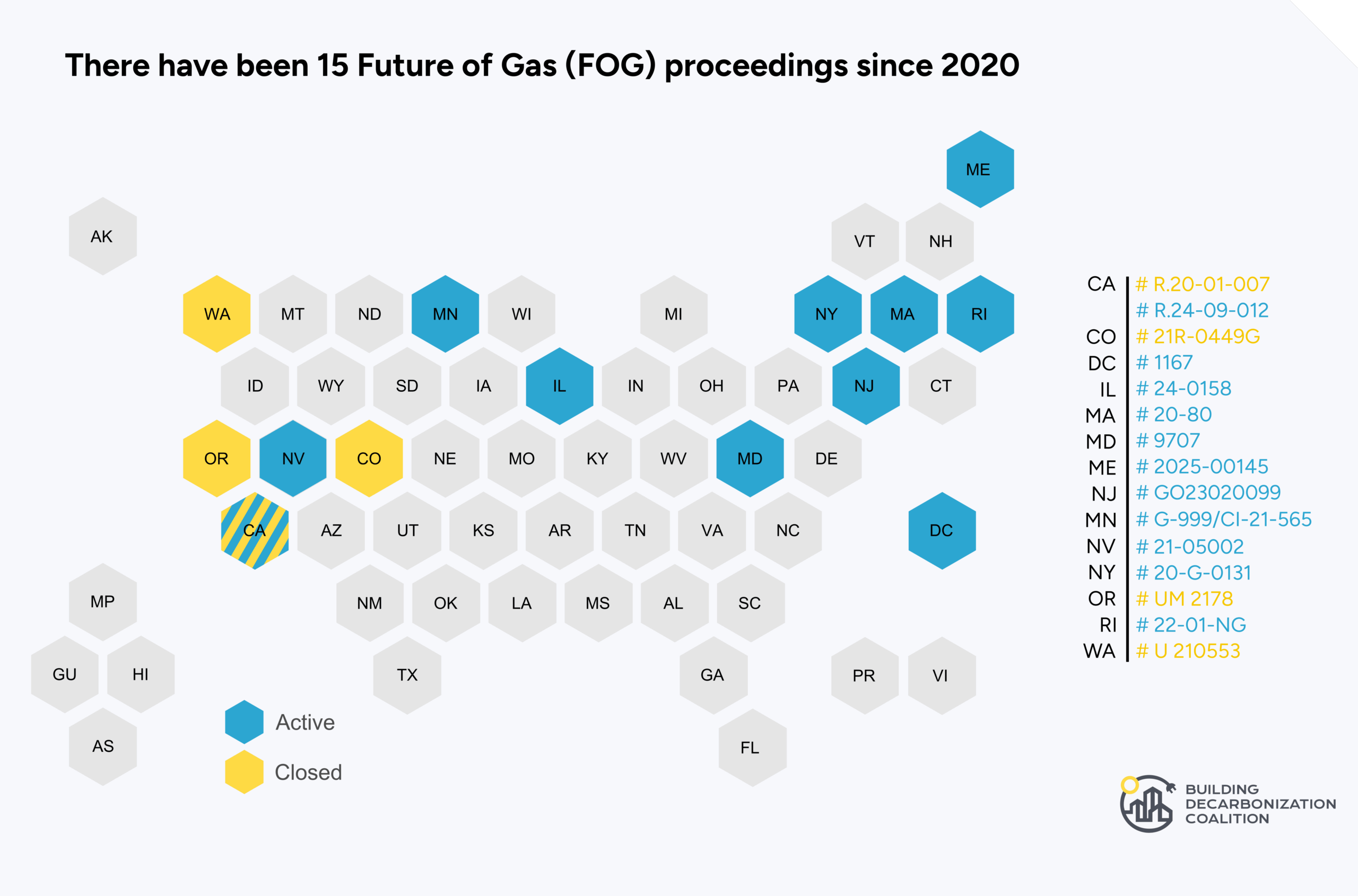

Future of Gas Proceedings

Since 2020, 15 proceedings that we consider to address the future of gas have been opened across 13 states and D.C. Currently, 11 proceedings are active, though not all have had recent activity. These proceedings have led to key insights on the inequitable distribution of methane pollution, the risks of business-as-usual gas system growth, and the urgency of reforming outdated policies. A managed, neighborhood-scale transition off the gas system requires clear decarbonization targets to halt expansion, limit reinvestment, and right-size the system.

For a comprehensive list of Future of Gas proceedings, including closed and inactive dockets, see BDC’s public tracker.

The “Future of Gas” is an evolving policy framework used to describe the questions, assumptions, and arguments surrounding the long-term sustainability of the methane gas system. Researchers, state energy offices, legislators, and utility regulators have used the phrase to describe policies, reports, and proceedings since at least 2019. Advocates have also applied it retroactively to highlight the growing number of regulators and legislators critically examining the gas system’s longevity.

Figure 8: Summary of Future of Gas proceedings

Q1 Future of Gas Proceeding Highlights:

- The managed gas transition is moving from policy direction to regulatory decision-making: California has designated 151 potential neighborhood decarbonization zones; Massachusetts is adjudicating line extension allowances and service obligations; and Maryland has entered the testimony phase of its Future of Gas proceeding.

- Who pays for the gas transition is emerging as the defining policy question: California is developing rules for pilot cost recovery and cost allocation; Massachusetts and Maryland are both moving to eliminate gas line extension subsidies; and Maryland’s Future of Gas proceeding is also building the record on stranded asset risk, gas system expansion, and long-term ratepayer impacts.

- Utilities are increasingly required to justify gas pipeline investments against non-gas-pipeline alternatives: Utilities in New York are filing a geographically specific NPA proposals and Massachusetts and Maryland are embedding NPA standards into long-term gas planning.

- The “obligation to serve” gas is being reexamined under climate law: Massachusetts is evaluating whether gas service may be retired without unanimous consent; Maryland’s Future of Gas proceeding is examining potential limits on system expansion and how climate statutes affect long-term gas planning; and D.C. stakeholders are pressing for climate-aligned gas planning and a reassessment of Washington Gas’s long-term role under the District’s climate laws.

- Regulators are developing the analytical tools needed for long-term gas system transition planning: Maine is developing a structured GHG evaluation matrix; Minnesota has established the carbon-cost scenarios utilities must use in their first gas IRPs; and Illinois commissioned a statewide decarbonization pathways study to establish comparable cost and scenario modeling across utilities.

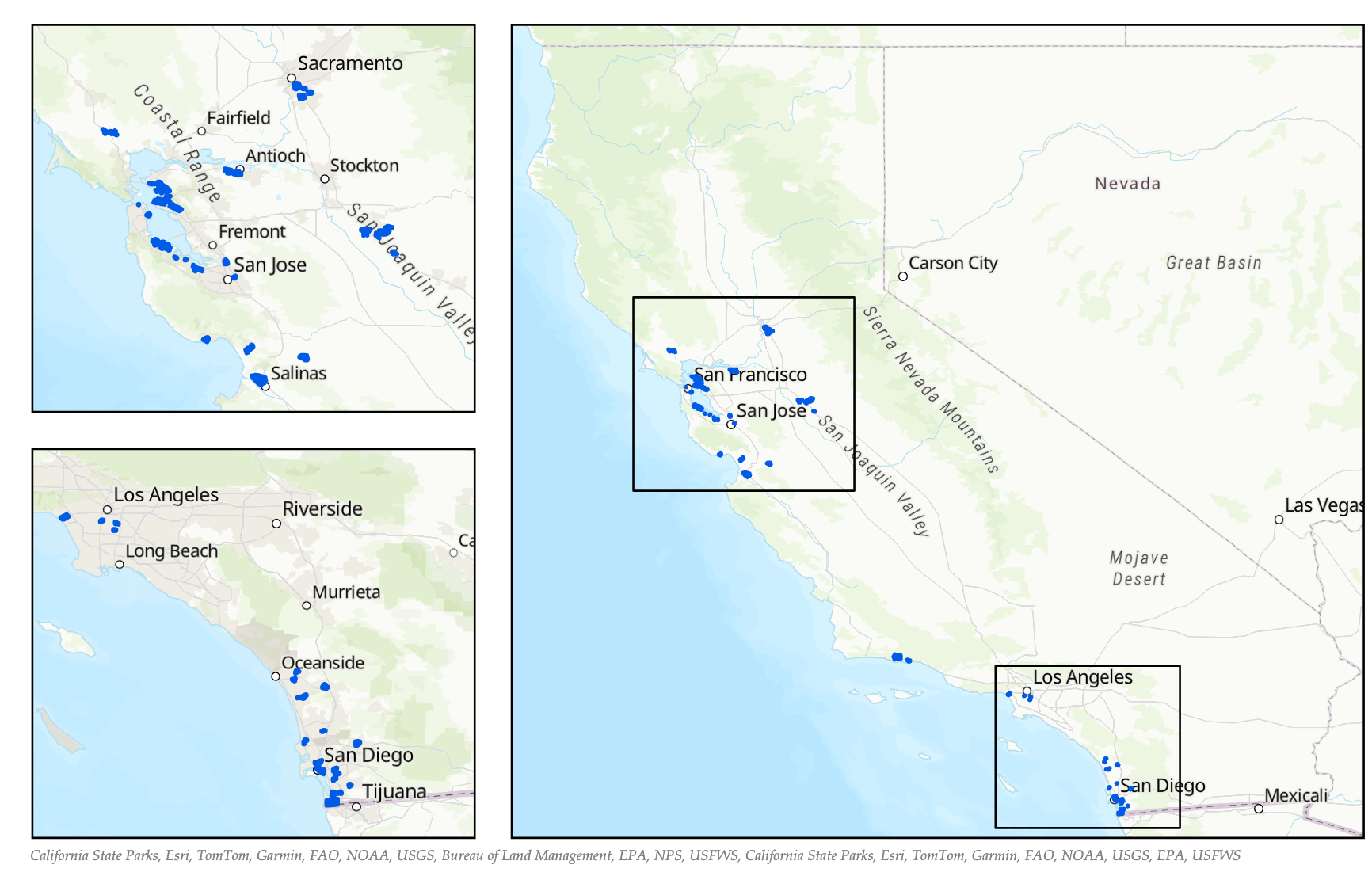

Figure 9: Initial SB 1221 Neighborhood Decarbonization Zones, 2025

Source: CPUC Decision 25-12-042, Appendix B.

Q1 FOG Proceeding Activity

|

State |

Recent Activity |

|

California Order Instituting Rulemaking to Establish Policies, Processes, and Rules to Ensure Safe and Reliable Gas Systems in California and Perform Long-Term Gas System Planning (R. 24-09-012) (Part 2, 2024-present under 24-09-012) (Part 1, 2020-2024 under R.20-01-007) |

The CPUC’s “Future of Gas Part 2” rulemaking (R.24-09-012) is intended to guide California’s long-term transition away from the gas system while advancing near-term decarbonization actions. The proceeding implements SB 1221 (2024), which authorizes up to 30 voluntary neighborhood-scale decarbonization pilots and modifies the gas “obligation to serve” by allowing utilities, with CPUC approval, to reduce the customer consent threshold to no less than 67%. The rulemaking is structured in phases addressing interim actions, long-term gas planning, and SB 1221 implementation, including required mapping of planned pipeline replacements and designation of priority decarbonization zones. In 2025, utilities submitted 10-year pipeline replacement maps and proposed priority zones, drawing criticism from advocates for lacking sufficient building-level and customer data to enable meaningful community engagement. In December, the CPUC designated 151 initial Priority Neighborhood Decarbonization Zones (PNZs) at the census tract level, prioritizing areas with demonstrated local support and a significant concentration of planned gas main replacements, and supplementing them with high-scoring environmental and social justice communities. The Commission emphasized that these are “initial” zones and committed to updating them by the end of 2026, while requiring utilities to conduct outreach and host public information sessions in early 2026. Workshops throughout the year also focused on advancing non-pipeline alternatives (NPAs), including cost-effectiveness and cost recovery frameworks. The Commission must now establish clear NPA and pilot selection policies ahead of the July 2026 deadline for utilities to apply to run neighborhood-scale decarbonization pilots. Planned Pipeline Replacement Maps:

Q1 2026: Priority Neighborhood Decarbonization Zones (PNZs)

Outreach: Utilities must perform outreach to affected communities in the PNZs and document compliance and outreach efforts by April 1, 2026. Third Amended Scoping Memo (March 2026)

ALJ Ruling on Cost Recovery (March 2026)

CSU Monterey “Lessons Learned” Report

What’s Next:

|

|

D.C. In the Matter of the Implementation of Electric and Natural Gas Climate Change Proposals (FC # 1167) (2020-present) Related docket on integrated system planning: FC #1182 |

The DC Public Service Commission (DCPSC) opened Formal Case No. 1167 in 2020 following the AltaGas–Washington Gas Light (WGL) merger, after required climate business plans were deemed insufficient to demonstrate alignment with the District’s climate goals. Guided by the expanded mandate of the 2018 CleanEnergy DC Omnibus Act, the proceeding examines whether utilities are meeting the District’s energy and climate commitments. In response to Order No. 22313 (Oct. 2024), which required revised 15-year Climate Solutions and Climate Business plans, advocates urged the Commission to adopt Integrated Distribution System Planning (IDSP) and to separate electric and gas planning into distinct dockets. The PSC subsequently opened a new IDSP docket (FC-1182) while continuing the Future of Gas inquiry under FC-1167 (Order No. 22339). In March 2026, the PSC also opened the Integrated Natural Gas Distribution System Planning (“INGDSP”) for gas utilities (FC-1187). In 2025, the Commission advanced both proceedings. It established an IDSP working group focused on load forecasting, DER transparency, resilience, electrification, and equity, with a report due in April 2026. Meanwhile, WGL filed its 15-year gas emissions reduction plan in the Future of Gas docket, drawing criticism from the Office of People’s Counsel and Sierra Club for failing to demonstrate meaningful emissions reductions, adequately incorporate electrification, or fully assess customer and climate impacts. Q1 2026: Procedural Developments

Gas Planning Reform Proposal

Coordination & Implementation Oversight

Cost Allocation & Governance Questions

What’s Next:

|

|

Illinois The Future of Natural Gas and issues associated with decarbonization of the gas distribution system (Docket # 24-0158) (2024-present) |

In March 2024, the ICC launched a statewide Future of Gas proceeding to examine how Illinois gas utilities’ infrastructure plans align with the state’s decarbonization and electrification goals. Following initial workshops in 2024, Phase 2 is now underway, culminating in a report due in early 2026. Phase 2B (March 2025) established two working groups: one narrowed more than 100 proposed decarbonization pilots (including neighborhood electrification, thermal energy networks, industrial heat pumps, and alternative fuels), while the other is evaluating pathway feasibility and economic impacts. Q1 2026: Procedural Developments

Decarbonization Pathways Study

Legislative & Regulatory Reform (Phase 2C)

Gas Planning Governance Shift

What’s Next:

|

|

Maine Inquiry Regarding Future of Natural Gas (Case No. 2025-00145) (May 2025-present) |

The Maine Public Utilities Commission (MPUC) opened a new Future of Gas proceeding to examine how gas utility regulation should align with the State’s statutory greenhouse gas reduction goals (Notice of Inquiry). Maine law requires economy-wide emissions reductions of 45% by 2030 and 80% by 2050 (from 1990 levels), and carbon neutrality by 2045. The Commission is tasked with facilitating emission reductions consistent with these targets while ensuring safe, adequate, and reasonably priced service. The inquiry seeks to develop a framework to evaluate the climate impacts of gas infrastructure investments and supply commitments, assess alignment with state climate targets, and examine potential future pathways for methane gas. Initial scope comments (June 2025) revealed a clear split among stakeholders: gas utilities emphasized renewable natural gas (RNG) and hydrogen, while the Office of the Public Advocate, the Governor’s Energy Office, and labor and climate groups supported exploration of thermal energy networks (TENs) and other non-pipeline alternatives. In 2026, the proceeding shifted from high-level inquiry to active framework development, with the Commission considering adoption of a structured evaluation methodology to guide future gas investment decisions. Q1 2026: Initial Workshop (Jan. 21, 2026)

OPA Proposed Evaluation Matrix

The Workshop discussion focused on whether to formalize climate-aligned evaluation criteria, how to compare alternatives consistently, and how to integrate stranded asset and rate impact analysis into decision-making. Post-Workshop Procedural Order (Feb. 13, 2026)

What’s Next:

|

|

Maryland New: Case No. 9707 (First petition filed in Feb. 2023; second petition in May 2025; Order 91791 to open Future of Gas investigation within docket issued in August 2025)

|

In February 2023, Maryland’s Office of People’s Counsel (OPC) petitioned the Public Service Commission (PSC) to open a Future of Gas proceeding to evaluate whether gas utility planning, practices, and rates remain “just and reasonable” and consistent with the public interest (pg. 7). Following public comments in 2024 and a renewed OPC petition in 2025, the PSC issued an order on June 13, 2025 signaling its intent to eliminate gas line extension allowances (LEAs) for new connections. The PSC reasoned that subsidies encouraging gas system expansion may conflict with Maryland’s climate goals and obscure the true cost of gas service. Staff were directed to propose LEA regulations by December 1, 2025, to be addressed through Rulemaking 92. On August 20, 2025, the PSC formally opened a comprehensive Future of Gas proceeding (Order 91791) within Case No. 9707 to examine the long-term role of natural gas in light of Maryland’s greenhouse gas reduction and electrification commitments. Citing the Climate Solutions Now Act and the Next Generation Energy Act, the Commission will evaluate:

Q1 2026: Procedural Developments:

Line Extension Allowance Reform:

Comments on Draft LEA Regulations Dozens of comments were filed in support or opposition of the proposed LEA reforms.

What’s Next (Future of Gas [#9707] & LEA Reform [RM 92])

|

|

Massachusetts The Future of Gas (Docket #: 20-80) (2020-present) Utility Climate Compliance Plans: (25-40, 25-41, 25-42, 25-43, 25-44, 25-45) |

In its landmark December 2023 order in the “Future of Gas” docket, the Massachusetts Department of Public Utilities (DPU) established a new standard for gas system investment consistent with the state’s net-zero by 2050 mandate. The DPU shifted the burden of proof to gas utilities, requiring them to demonstrate that non-pipeline alternatives (NPAs) are either not cost-effective or infeasible before proceeding with major gas infrastructure investments, including full pipeline replacements. This marked a departure from business-as-usual gas expansion and laid the groundwork for reassessing long-term stranded asset risk and ratepayer exposure. In 2024, the DPU turned to reforming gas line extension allowances (LEAs). Utilities were directed to report on their LEA practices, and in a February 5, 2025 memorandum, the Department proposed eliminating LEAs by requiring new customers to pay the full cost of connecting to the gas distribution system. The proposal further stated that “no costs associated with a new service or line extension shall be deemed prudently incurred and, thus, eligible for inclusion in an LDC’s rate base” (Feb. 5, 2025 Memorandum). Implementation is occurring through the 2025 Climate Compliance Plan (CCP) dockets (D.P.U. 25-40 through 25-45), covering Eversource, National Grid, Liberty, and Unitil. In a subsequent Interlocutory Order, the DPU proposed a simplified policy to eliminate LEAs and clarified that final determinations would be made within these CCP dockets. Utilities sought a stay, citing procedural concerns, but the Department directed them to file revised tariffs by October 20, 2025 reflecting removal of LEAs. At the same time, the Department is evaluating how the state’s 2024 climate law (S. 2967) reshapes the gas “obligation to serve,” including whether utilities may retire gas service in favor of electrification or thermal energy networks, and whether neighborhood-scale decarbonization projects can proceed without unanimous customer consent. The central question is whether the obligation to serve guarantees indefinite gas service upon request, or whether the DPU may permit targeted retirement of gas infrastructure where adequate non-gas alternatives exist. This issue is critical to whether neighborhood-scale electrification or thermal energy network projects can proceed without unanimous customer consent. Q1 2026:

Obligation to Serve:

What’s Next (LEAs & Obligation to Serve)

|

|

Minnesota In the Matter of a Commission Evaluation of Changes to the Natural Gas Utility Regulatory and Policy Structures to Meet State Greenhouse Gas Reduction Goals (Docket #: G-999/CI-21-565) (2021-present) |

In 2021, the Minnesota Legislature directed the Public Utilities Commission (PUC) to evaluate changes to natural gas regulatory structures needed to meet or exceed the state’s greenhouse gas reduction goals. The Commission opened the Future of Gas docket (G999/21-565) to implement this directive. Much of the early work proceeded through gas utilities’ Integrated Resource Plan (IRP) proceedings, culminating in March and October 2024 orders addressing modeling assumptions, emissions pathways, and planning transparency. In January 2025, the Commission reset the scope and timeline, returning focus to the Future of Gas docket. Current informational hearing topics include winter reliability, renewable natural gas (RNG), hydrogen and other alternative fuels, hybrid heating rate design, and updates from the Thermal Energy Network (TEN) Work Group. In parallel, the Commission initiated review of gas line extension allowance (LEA) policies before a comment period evaluating changes to rates to promote heat pump affordability and evaluate and address stranded asset risks as a result of electrification. The LEA comment period closed September 9, 2025, with a decision still pending. The rate and stranded asset comment period will follow at an undetermined date. Q1 2026: Regulatory Cost of GHG Emissions (Gas IRPs – Xcel, CenterPoint, MERC):

Thermal Energy Network (TEN) Work Group:

What’s Next:

|

|

New York Proceeding on Motion of the Commission in Regard to Gas Planning Procedures (Docket # 20-G-0131) (2020-present)

|

The New York gas planning docket (20-G-0131) originated in response to gas moratoria concerns but has since evolved into a statewide framework for managed gas transition planning. The PSC now requires each gas utility to file a Long-Term Gas Plan (LTGP) every three years in separate utility-specific dockets. Each LTGP must include at least one scenario with no new traditional gas infrastructure, quantify greenhouse gas impacts, evaluate non-pipeline alternatives (NPAs), and provide updates on demand forecasts, electrification progress, and system risks. In 2025, utilities submitted updated LTGPs and annual reports reflecting expanded electrification and NPA strategies. The Commission intensified scrutiny, issuing directives to curb gas demand growth, strengthen NPA deployment, improve forecasting methodologies and bill impact analyses, and align long-term planning more closely with New York’s Climate Leadership and Community Protection Act (CLCPA) mandates. Q1 2026: Central Hudson Gas & Electric (23-G-0676): Targeted NPA Implementation (End of 2025):

New York State Electric & Gas Corporation and Rochester Gas and Electric (23-G-0437):

ConEd and Orange and Rockland Utilities (23-G-0147):

National Grid (24-G-0248):

National Fuel Gas Distribution Corp. (22-G-0610):

Liberty Utilities (St. Lawrence Gas) Corp. (20-G-0131):

What’s Next (Long-Term Gas Plans)

|

Future of Heat Regulation

Q1 Highlights

- California is piloting a tariff-on-bill financing model designed to electrify homes without relying on traditional consumer loans, with the goal of expanding access to clean energy upgrades for renters and lower-income households who face upfront cost and credit barriers.

- Massachusetts is shaping utility rate design around affordability and electrification through its seasonal heat pump rate, new energy-burden-based bill protections, and a proposed geothermal service rate to scale thermal energy networks within gas planning.

- New York is deploying low- and moderate-income programs for electrification and energy efficiency through 2030

- Maryland is advancing clean heat on two fronts with a Clean Heat Standard for fuel suppliers and a zero-emission heating equipment standard to establish both emissions accountability and long-term market transformation in the thermal sector.

- The D.C. PSC has scaled down Washington Gas’s accelerated pipeline replacement plan while opening a new integrated gas system planning docket to complement the District’s existing electric system planning and Future of Gas proceedings.

|

State / Rule or Regulation |

Recent Activity |

Category |

|

California, Rulemaking Regarding Building Decarbonization (R. 19-01-011) (2019-present) |

The Building Decarbonization Rulemaking was opened in 2019 following the passage of SB 1477, which provided cap-and-invest funding for two building electrification pilot programs: the Building Initiative for Low-Emissions Development (BUILD) Program and the Technology and Equipment for Clean Heating (TECH) Initiative. The proceeding has since evolved beyond oversight of the original pilot programs into a broader forum for implementation lessons, zonal decarbonization concepts, and coordination across related CPUC proceedings. Activity at the end of 2025 and beginning of 2026 focused on procedural extensions, PG&E’s CSU Monterey Bay zonal electrification “lessons learned” report, and a Commission-convened workshop on best practices and future pathways for scaling building decarbonization. PG&E’s March 2026 workshop report underscores that the proceeding is now being used to surface cross-cutting implementation barriers, such as customer complexity, workforce constraints, remediation needs, affordability concerns, and the need for better coordination across funding streams, grid planning, and related rulemakings. Q1 2026:

What’s Next:

|

line extension allowances, rebates and incentives; grid management; workforce |

|

California, OIR to Investigate and Design Clean Energy Financing Options for Electricity and Natural Gas Customers |

Rulemaking 20-08-022 was instituted in 2020 to evaluate financing strategies that could support larger-scale investments in clean energy improvements. In 2023, the CPUC directed utilities to propose expanded tariff-on-bill (TOB) financing programs—sometimes referred to as Inclusive Utility Investment (IUI)—which allow customers to repay the cost of clean energy upgrades, such as heat pumps, through a charge on their monthly utility bill rather than paying the full cost upfront. The model is designed so that projected energy savings offset the incremental on-bill charge, lowering upfront barriers and expanding access to electrification, particularly for renters and lower-income households. In 2024, the IOUs submitted a joint TOB proposal, which was evaluated by a third party and released for stakeholder comments in May 2025. Ultimately, only Southern California Edison’s pilot was approved. The proceeding was closed following the final decision in December 2025. Q1 2026: Proposed Decision (Issued October 31, 2025)

Key Elements of the Approved (Modified) SCE Pilot

Comments on Proposed Decision

Final Decision

What’s Next:

|

inclusive utility investment, tariff-on-bill, clean energy financing, equity |

|

California OIR for Oversight of Energy Efficiency Portfolios, Policies, Programs, and Evaluation. |

Natural Gas Energy Efficiency Incentives Policy In April 2025, the CPUC opened R.25-04-010 as the successor to the long-running energy efficiency rulemaking, establishing a new forum for oversight of energy efficiency portfolios, cost-effectiveness policy, and program administration. Of central concern is the reconsideration of ratepayer-funded incentives for gas-burning appliances. In late 2025, staff proposed further phasing out gas EE incentives where viable electric alternatives (VEAs) exist. Q1 2026:

What’s Next:

|

gas subsidies, energy efficiency |

|

Colorado, Black Hills Clean Heat Plan (23A-0633G) |

A January 2025 Decision by the Colorado Public Utilities Commission marked a pivotal moment in the state’s Clean Heat Plan implementation, raising the question of whether a gas-only utility can be required to meaningfully pursue beneficial electrification (BE) alongside traditional gas efficiency programs. The case stems from Colorado’s 2021 Clean Heat statute (SB21-264), which requires gas utilities to reduce greenhouse gas emissions through approved clean heat portfolios. Q1 2026: Procedural Developments

Second Settlement Agreement

Key Dispute

What’s Next:

|

clean heat standards, electrification, managed gas transition |

|

D.C. In The Matter Of The Investigation Into Washington Gas Light Company’s Strategically Targeted Pipe Replacement Plan |

Washington Gas Light’s accelerated pipeline replacement program (formerly ProjectPIPES) remains under active scrutiny as the District weighs safety, climate alignment, and ratepayer risk. In December 2022, WGL filed its PIPES 3 proposal, a five-year, $671.8 million plan. In June 2024, the Public Service Commission of the District of Columbia (DC PSC) dismissed it, directing the utility to refocus on high-risk pipe replacement and better align with the District’s climate goals. WGL refiled in September 2024 as the Strategic Accelerated Facility Enhancement (SAFE) Plan, proposing $215 million over three years to replace 12.4 miles of main and 3,608 service lines, with continued recovery through the existing surcharge mechanism. Consumer advocates argued the revised plan still failed to adequately evaluate non-pipeline alternatives (NPAs), including electrification, and did not sufficiently address stranded asset risk. Rather than approving SAFE immediately, the Commission extended the existing surcharge through the end of 2025 with a $34 million spending cap and moved the case into an evidentiary phase focused largely on WGL’s JANA risk model. In March 2026, the Commission approved a modified SAFE plan, cutting WGL’s proposed budget by roughly 30 percent and imposing tighter annual caps, threshold-based cost recovery, and enhanced reporting requirements. At the same time, it opened a new Integrated Natural Gas Distribution System Planning proceeding (“INGDSP”, Case # 1187), signaling that future gas replacement spending will be evaluated within a broader long-term gas planning and decarbonization framework. Q1 2026:

What’s Next:

|

accelerated pipeline replacement, NPAs |

|

D.C. Integrated Distribution System Planning (“IDSP”) |

The D.C. PSC opened Formal Case No. 1182 in late 2024 to create a more coordinated, transparent, and climate-aligned framework for electric distribution planning. The docket responds to long-running concerns that Pepco’s planning, load forecasting, and DER integration processes are too fragmented and insufficiently aligned with the District’s clean energy goals. In July 2025, the Commission directed that an IDSP Working Group be convened to develop recommendations on load forecasting, data transparency, DER valuation and hosting capacity, and resilience, electrification, and equity. Q1 2026:

What’s Next:

|

Integrated system planning, electric system |

|

Illinois Informal Process following Docket No. 24-0081, Illinois Commerce Commission

|

Following the ICC’s February 2025 order requiring Peoples Gas to evaluate non-pipeline alternatives (NPAs) as part of its pipeline replacement strategy, an independent facilitator convened a seven-part workshop series between September and December 2025. The final summary report synthesizes workshop discussions, stakeholder proposals, and areas of agreement and disagreement. This process represents Illinois’ most formal effort to date to evaluate how non-pipeline alternatives could be integrated into Peoples Gas’ pipeline replacement planning. Q1 2026: Workshop Outcomes & Key Themes Stakeholder NPA Proposals Presented

Candidate Identification & Near-Term Actions

Affordability Debate Over Gas Line Extensions

Community Engagement

Workshop Takeaways The workshop process did not produce consensus on immediate NPA implementation but did:

What’s Next:

|

non-pipeline alternatives |

|

Maryland |

Governor Wes Moore’s 2024 Executive Order established a Clean Heat Standard (CHS) requiring Maryland’s thermal sector to reduce emissions from heating delivery services and transition to clean heating technologies, including zero-emission equipment (e.g., heat pumps), weatherization, and cleaner fuels. A foundational component of the policy is The Heating Fuel Provider Program Rule, which creates the data infrastructure necessary to set enforceable emissions reduction targets. Q1 2026: Heating Fuel Provider Reporting Rule Finalized (Dec. 2025)

What’s Next:

|

clean heat standards, electrification |

|

Maryland |

Following Governor Moore’s 2024 Executive Order, the Maryland Department of the Environment (MDE) began developing regulations to phase out fossil fuel heating equipment and address harmful nitrogen oxides (NOx) and greenhouse gas (GHG) emissions from the building sector. MDE is jointly developing the rule with the Northeast States for Coordinated Air Use Management (NESCAUM), using the 2024 NESCAUM Model Rule as a foundation. The regulation, known as the Zero-Emission Heating Equipment Standard (ZEHES), is intended to transition Maryland’s heating market toward zero-emission technologies while incorporating flexibility and consumer protections. Q1 2026: Rule Design Advancing (Dec. 2025)

Contractor Working Group Launched

Scope Considerations Expanding

Equity & Program Alignment

What’s Next:

|

electrification, equipment standards |

|

Massachusetts Eversource Geothermal Rate Case (DPU 25-86) |

On September 17, 2025, NSTAR Gas (Eversource Energy) filed a petition seeking approval of a regulatory framework and new geothermal rate to develop networked geothermal systems in new construction projects in its service territory. The filing follows the Department’s 2023 policy decision in D.P.U. 20-80-B and recent statutory changes that explicitly authorize gas companies to make, sell, or distribute networked geothermal energy. The proposal seeks to establish a structured process for evaluating geothermal alongside natural gas in new developments and to create a dedicated geothermal rate for participating customers. Under the proposed framework:

The filing is structured as a Tier 2 proceeding and includes testimony from both a Geothermal Panel and a Rates Panel. Q1 2026:

What’s Next:

|

thermal energy networks, rates |

|

Inquiry by the Department of Public Utilities on its own Motion into Energy Burden with a Focus on Energy Affordability for Residential Ratepayers |

In January 2024, the Massachusetts Department of Public Utilities (DPU) opened an inquiry to examine residential energy burden and improve affordability for electric and gas customers. “Energy burden” is defined as the share of a household’s annual income spent on utility bills; for example, a 4% energy burden target means combined annual electric and gas bills are calibrated not to exceed roughly 4% of household income under modeled usage assumptions. Following extensive stakeholder comments, workshops, technical sessions, and model development, the DPU issued a Phase I Order on February 17, 2026 establishing a new statewide framework for tiered low-income discount rates. The Order represents a structural shift from flat percentage discounts to an income-tiered model explicitly tied to target energy burdens. Q1 2026: Phase I Order (Feb. 17, 2026)

Energy Burden Targets Embedded in Rates

Discount Floors

Implementation & Phase-In Protections

RAAF Reform (Cost Recovery Shift)

Moderate-Income Discount (Next Phase)

What’s Next:

|

rates, affordability, energy burden |

|

New York, Energy Efficiency and Building Electrification proceedings 14-M-0094: Proceeding on Motion of the Commission to Consider a Clean Energy Fund 18-M-0084: In the Matter of a Comprehensive Energy Efficiency Initiative 25-M-0248: In the Matter of the 2026-2030 non-Low- to Moderate-Income Energy Efficiency and Building Electrification Portfolio 25-M-0249: In the Matter of the 2026-2030 Low- to Moderate-Income Energy Efficiency and Building Electrification Portfolio |

The Energy Efficiency and Building Electrification proceeding, formerly referred to as “New Efficiency: New York (NE:NY),” is the state’s $5 billion portfolio of ratepayer-funded energy efficiency and electrification incentive programs. These offerings were under regulatory review by the NYS Public Service Commission to improve program design, spending, and accountability. On May 15, 2025, the Commission established two new proceedings—one for Low- and Moderate-Income (LMI) programs (25-M-0249) and one for market-rate programs (25-M-0248)—authorizing approximately $1 billion per year for 2026–2030 in energy efficiency and clean energy solutions, including building electrification. Administered by the state’s investor-owned electric and gas utilities and NYSERDA, nearly one-third of the funding ($1.57 billion) is dedicated exclusively to LMI programs. Following the May 2025 orders, the Commission advanced implementation of the broader Clean Energy Fund (CEF), including approval of the 2026–2030 Innovation & Research (I&R) portfolio and modifications to the New York Green Bank (NYGB). Together, these actions shape the innovation, financing, and market infrastructure supporting building electrification through 2030. Q1 2026: Clean Energy Fund (14-00549) Procedural Developments

Innovation & Research Portfolio (Oct. 2025)

NY Green Bank Modifications (Jan. 2026)

Market-Rate / Non-LMI Programs (25-M-0248) Procedural Developments

Implementation Updates

LMI Programs (25-M-0249) Procedural Developments

Implementation Oversight

What’s Next: LMI and Non-LMI Programs

Clean Energy Fund

|

energy efficiency, electrification, LMI programs |

|

New York, Utility Thermal Energy Network and Jobs Act (UTENJA) 22-M-0429 |

Since being directed by the 2022 UTENJA law, New York utilities have been exploring how they can use thermal energy networks to decarbonize entire neighborhoods across the state. There are currently 10 proposed pilot projects under PSC review. The proceeding has moved from feasibility analysis to detailed engineering design, lifecycle cost validation, and customer protection planning, positioning several pilots for potential Stage 3 construction decisions. Q1 2026: Procedural Developments

Engineering & Cost Analysis

Stakeholder Comments

What’s Next:

|

thermal energy networks, workforce, neighborhood scale |

VI. Looking Ahead

What to watch for in the year ahead

- The heat pump crossover could signal a lasting market shift. In 2026, we will see whether heat pumps can continue to outsell air conditioners.

- The refrigerant transition will shape the HVAC market this year. With higher-GWP equipment phased out as of January 1, 2026, the coming months will show how smoothly manufacturers, contractors, and consumers navigate the transition.

- Future of Gas proceedings continue to advance. In California, Massachusetts, Maryland, New York, and D.C., regulators are increasingly being asked not just to study the gas transition, but to make real decisions about planning, rates, and future investment.

- Neighborhood-scale transition pilots are getting closer to real implementation. In California, utilities are expected to submit plans for up to 30 neighborhood-scale decarbonization pilots beginning in July 2026, while New York’s UTENJA pilots are advancing toward Stage 3 construction decisions.

- Massachusetts is approaching decisions on two of the country’s most consequential gas reforms. Regulators are expected to decide whether to eliminate gas line extension subsidies and how far the state can reinterpret the gas “obligation to serve” under climate law—decisions that could determine whether neighborhood-scale transition projects can move forward without requiring unanimous customer consent.

- Maryland’s Future of Gas proceeding could help turn analysis into enforceable policy. This year will build the evidentiary record through testimony, rebuttal, and final statements, while the Commission also weighs reforms to gas line extension rules that would require new customers to pay the full cost of new gas hookups.

- D.C. is making notable progress on the managed gas transition. Alongside its Future of Gas proceeding and its recent move to scale back Washington Gas’s accelerated pipe replacement program, the District is now developing separate electric and gas planning processes that could help align long-term utility planning with climate goals.

- Affordability-focused reforms are continuing to take shape. Massachusetts utilities are preparing to implement new energy-burden-based discount rates, while New York continues refining its 2026–2030 electrification and efficiency portfolios. This year should also provide an early test of how Massachusetts’s new heat pump rate performs through its first heating season. These reforms will help show whether states are moving beyond clean heat ambition toward policies that actually lower costs and expand access.

VII. Methodology

- Heat pumps vs. furnaces and air conditioners: Data directly from AHRI monthly shipment reports, combining gas and oil furnaces into a single “fossil fuel furnaces” category.

- Gas utility spending: Data from AGA through 2023 (latest available). We establish the pre-2010 baseline by averaging inflation adjusted distribution spending from 1990-2009, then calculate the area between actual spend vs. baseline from 2011-2023 to get to $130 billion. In 2023, “excess” over the baseline is $20B, which we apply the 2-3x factor of ratepayer costs to get to “at least $40B” in lifecycle costs per year.

- Gas bill proportions: Using data from EIA, we compare total residential delivered cost of gas vs. citygate price. The citygate price is the commodity cost while the remainder cover delivery costs.

- Residential gas stats: From EIA, we plot residential gas consumption and consumers, adding a linear trendline for consumption over the plotted data and calculate the average annual growth of 0.9% for consumers over the plotted time period.