A quarterly update on the building decarbonization movement

Q2 | 2026

Authors

Kristin George Bagdanov, PhD, Associate Director of Research

Kevin Carbonnier, PhD, Associate Director of Analytics

About Our Research

BDC tracks and analyzes policies, trends, and data to accelerate the building decarbonization movement. We synthesize qualitative and quantitative data to produce rigorously researched, substantively contextualized, equitably cited, and endlessly shareable resources that help move our movement forward. We believe that research only becomes knowledge when it’s shared, so please pass along these resources to your communities and help us equitably decarbonize our buildings and neighborhoods. Read more about our research philosophy, resources, and reports.

Also, check out our Q1 | 2026 Momentum Report.

Table of Contents

I. The Big Picture

1. Overview

II. Market Momentum

1. Equipment Sales

2. Electric Heating in New Construction

3. Thermal Workforce

III. Neighborhood Scale

1. Project Highlight: Hayden, CO

2. Neighborhood-Scale Tools

IV. Gas System Costs and Affordability

1. Energy Affordability and Midterm Elections

V. The Thermal Transition

1. Legislation: Affordability and Consumer Protections

2. Line Extension Allowance Reform Update

3. Future of Gas Proceedings

4. Future of Heat Regulation

VI. Looking Ahead

VII. Methodology

I. The Big Picture

What happened this quarter in the building decarbonization movement

Repeated fossil-fuel price shocks are pushing consumers and policymakers toward local and affordable clean energy technologies. A recent article on Europe’s response to yet another global energy crisis captured both the immediate and longer-term effects these shocks are having on consumer behavior: “Europeans have responded to the price shock by rushing to line up heat pumps, solar panels and electric vehicles. They are hoping to lower their bills and reduce their reliance on imported fossil fuels.”

The desire for energy independence at both the household and system level has been pushing policymakers and consumers toward cleaner, more local, and less fuel-dependent alternatives. In the past year we’ve seen a growing trend in “balcony solar” bills, a hyperlocal and accessible way for households to offset rising electricity bills by generating a small share of their own power. Following trends in Europe, the U.S. saw 33 states with proposed bills to enable balcony solar this past session with eight states signing them into law so far (Canary).

For home heating and cooling, the desire to reduce dependence on volatile heating oil and natural gas has helped renew interest in heat pumps in Europe and grow the market in the U.S. According to new data released by the European Heat Pump Association, sales for heat pumps grew 10.3% percent in 2025 compared to 2024, rising from 2.38 million to 2.62 million units across 16 countries (EPHA). Recent reporting points to fossil fuel displacement as a primary driver of this increase in European markets, as the 2022 Russian invasion of Ukraine and now the war in Iran have demonstrated the consequences of fossil fuel dependency. In the U.S., heat pump sales have doubled over the past fifteen years, from 1.8M in annual shipments in 2010 to 3.64M in 2025, with a peak year of 4.3M in annual shipments in 2022 (BDC).

And rising gasoline prices due to the Iran war appear to be contributing to renewed consumer interest in EVs in the U.S. and abroad. While EV sales in the U.S. initially saw a post-tax-credit slump, recent data suggests that decline may be stabilizing, with May 2026 being the best month for EV sales since the end of the IRA tax credit. In Europe, surging petrol costs have helped accelerate demand for EVs, while China’s exports of EV and hybrids more than doubled in May compared to the prior year.

Across these technologies, there is a clear pattern emerging: people are looking for an off-ramp from fossil-fuel dependency, whether they are motivated by the climate crisis, economic pressure, energy security, or all three. This issue of Momentum explores where we’re seeing growth in the market, how policies are pushing electrification forward, and how concerns about energy affordability and energy bills are shaping our politics, especially the midterm elections.

Read on for the full report and download the executive summary below.

Overview

Here are the major events and actions shaping building decarbonization in the second quarter of 2026:

Market Momentum

- Heat pump shipments in the U.S. outpaced fossil fuel furnaces by 32% in the first quarter of 2026.

- There was only a 2% difference between heat pump and air conditioner sales in Q1 2026, the smallest Q1 gap recorded yet.

- In the U.S., heat pump sales doubled over the past 15 years.. In Europe, heat pump sales grew 10.3 percent across 16 European countries in 2025, compared to 2024.

- Electric heating in new construction has surpassed gas heating for five years running, reaching its highest point yet at 61% of the market share, compared to 38% for gas.

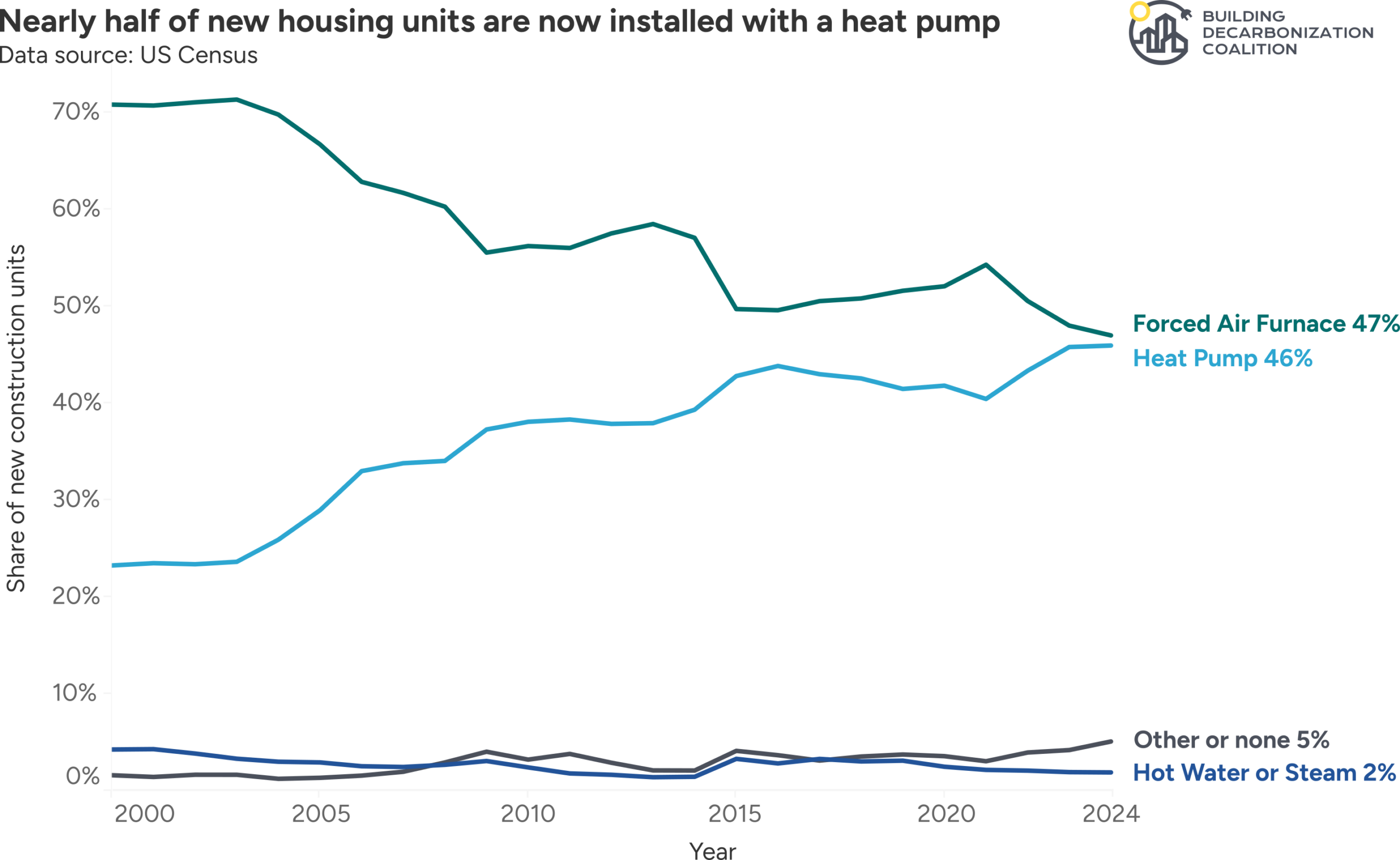

- Heat pumps are close to becoming the leading primary heating system in new homes. In 2024, 46% of new housing units were installed with a heat pump, nearly matching forced-air furnaces at 47%.

- KB Home builders, one of the largest U.S. home builders, has increased its all-electric home building by 18 percentage points over 4 years: it went from building 30% of its homes all-electric in 2021 to 48% in 2025.

- Enrollment in HVAC programs at two-year colleges has increased 64% in the last five years. Given the wave of expected retirements in the industry over the next decade, this growing interest from younger generations is critical for the success of the energy transition.

Energy Affordability

- Residential energy bills (includes gas and electric bills) rose by a median of roughly 17% across states from 2019 to 2024, with much sharper increases in some states.

- Gas and electric utilities across the U.S. are currently asking for more than $16B in rate increases, which would result in higher energy bills at a time when consumers are feeling stressed by inflation and rising costs.

- With 36 gubernatorial races and 22 public utility commissioner seats being voted on this year, energy affordability is becoming a central political issue heading into the midterms, with utility bills increasingly appearing in campaign debates over cost of living, utility profits, rate cases, data centers, climate policy, and corporate accountability.

- This year’s state legislative sessions have seen a host of new building decarbonization bills that are focused on energy affordability and consumer protections. So far we’ve tracking 22 affordability bills across 12 states; as of mid-June, 10 had passed, 6 remained in progress, and 6 had failed or were held during session.

Neighborhood-Scale Advancements

- Hayden, Colorado, shows how neighborhood-scale decarbonization can support economic transition in a fossil fuel-dependent community. The town is developing a municipally owned geothermal thermal energy network to serve a new 25-acre business district planned for roughly 230,000 square feet across 17 buildings.

- The California State University system released a new geothermal screening dashboard to help evaluate campus-level opportunities for networked geothermal systems, ranking sites based on infrastructure, geothermal conditions, and enabling factors.

- In New York, several utility thermal energy network pilots are awaiting determinations on whether they can move into Stage 3, which includes customer enrollment and construction.

- In Massachusetts, Eversource’s networked geothermal rate case could help define how gas utilities provide geothermal thermal service in new construction.

- In Colorado, regulators recognized that thermal energy networks can qualify as non-pipeline alternatives under gas planning rules, expanding the role TENs may play in avoiding unnecessary gas infrastructure investment.

The Future of Gas and Line Extension Allowance Reform

- Since 2020, 15 proceedings that address the future of gas have been opened across 13 states and D.C.; 11 remain active.

- California’s SB 1221 process is moving toward neighborhood-scale decarbonization implementation. The CPUC’s proposed decision would create three application rounds beginning December 15, 2026, assign pilot slots by utility, require utilities to show that gas infrastructure can be decommissioned, and establish customer outreach, consent, cost-effectiveness, and behind-the-meter cost recovery requirements.

- California’s line extension allowance (LEA) reforms are already showing results: in Q4 2025, all-electric residential new construction rates reached 73% for PG&E, 48% for SCE, and 68% for SDG&E.

- Illinois’ statewide LEA study found that existing ratepayers bear most gas line-extension costs under current utility practices, with new customer contributions ranging from 0% to roughly 33% and existing ratepayer responsibility exceeding 90% for several utilities. This evidence indicates high cross subsidization and counters the utility claim that existing ratepayers benefit from these new customer incentives.

II. Market Momentum

Demonstrating the durability of decarbonization

Equipment Sales

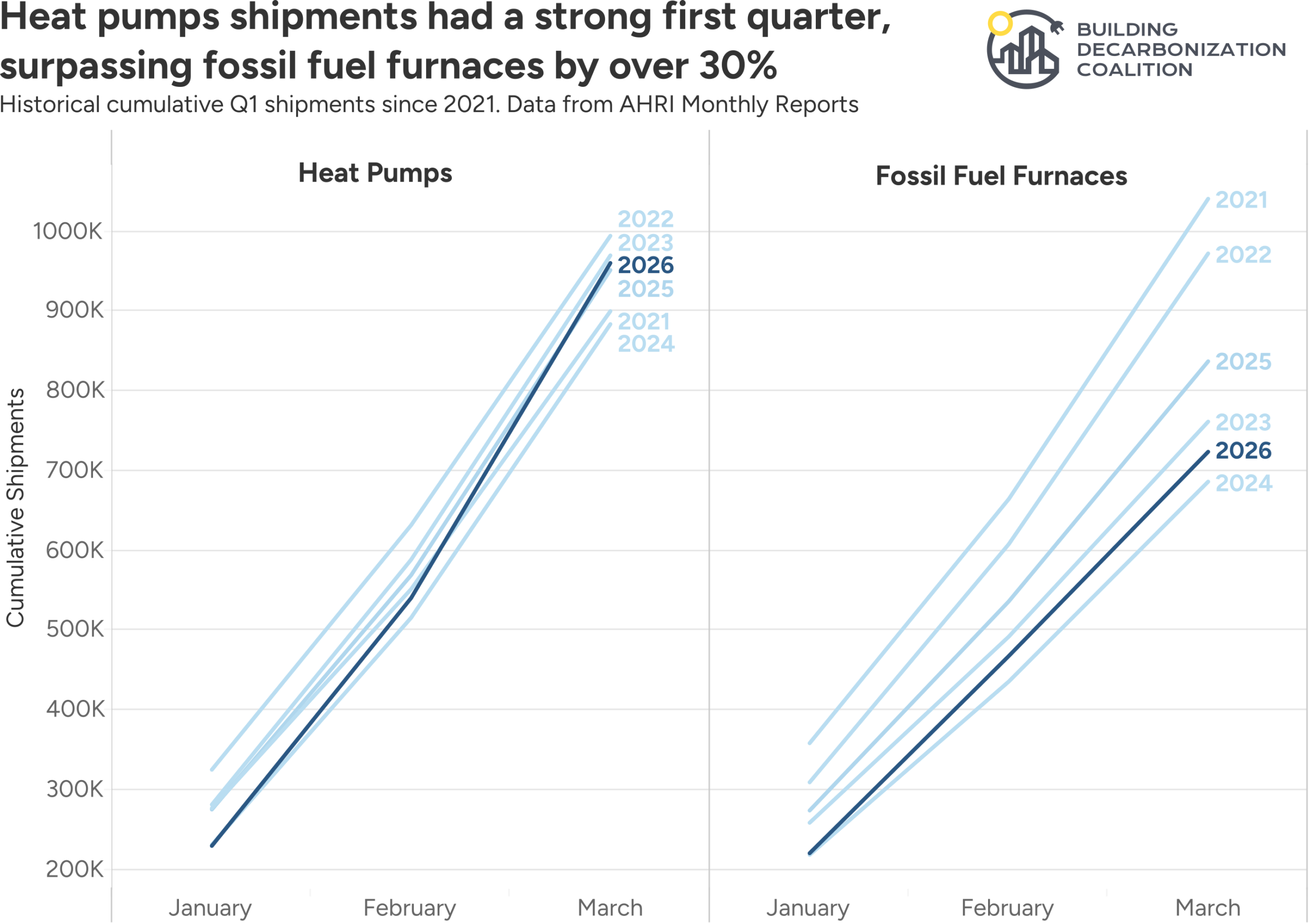

Heat pump shipments began 2026 with a strong first quarter. According to AHRI shipment data, heat pumps outpaced fossil fuel furnaces by 32 percent from January through March. That is especially notable because heat pump shipments are generally lower in the winter and tend to peak in the summer. We will be watching closely to see whether this early momentum carries into the warmer months, when shipment volumes typically rise.

Figure 1: Heat pump shipments in Q1 2026.

This momentum mirrors broader signs of market movement away from fossil fuel heating. Census data on heating fuels in new construction (discussed in the next section) has already shown heat pumps gaining ground in new homes, and the AHRI shipment data suggests that market momentum for electrifying heating remains strong so far in 2026.

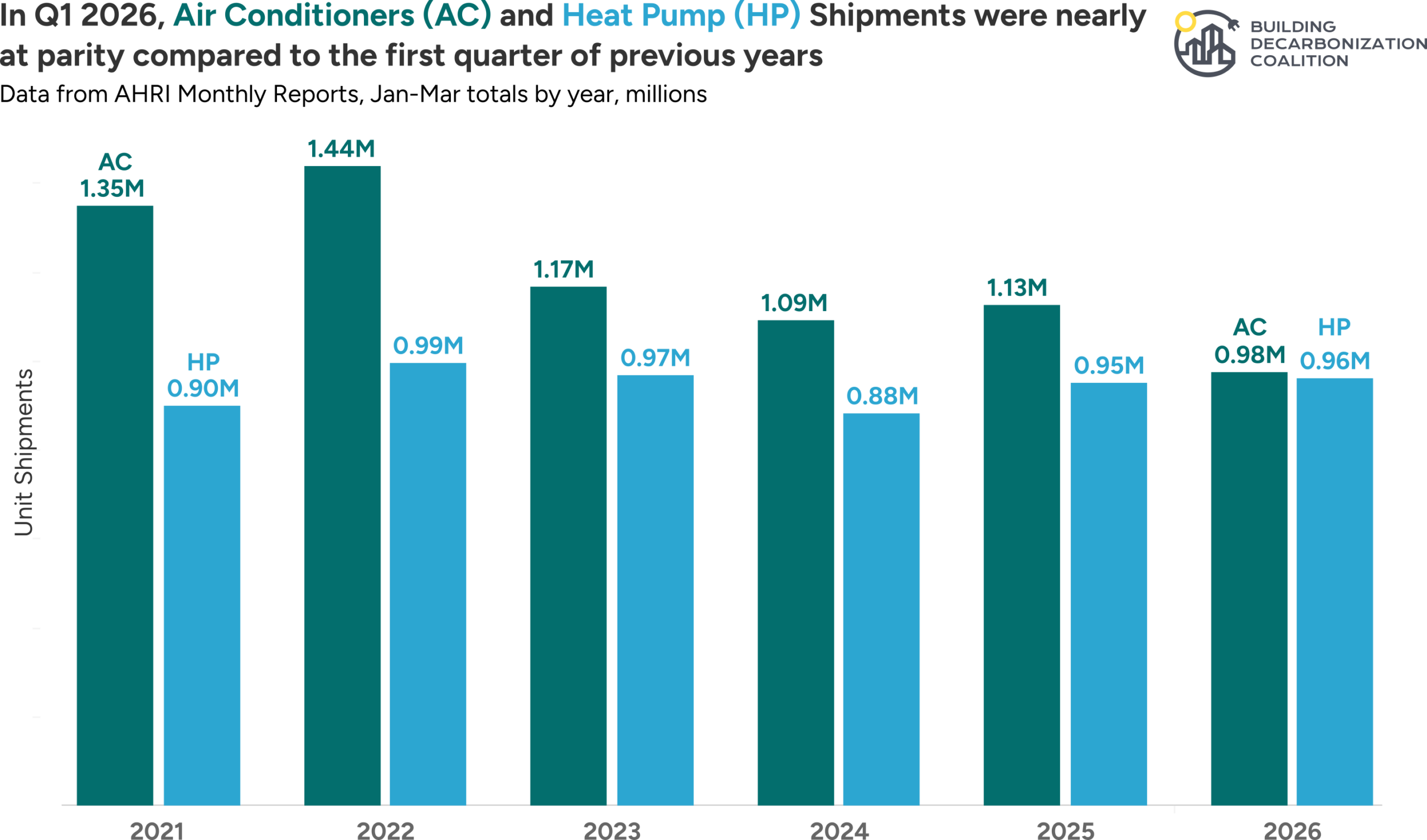

The same trend is visible in the relationship between air conditioner and heat pump shipments. In the first quarter of 2026, air conditioner and heat pump shipments were closer to parity than in any previous first quarter. Air conditioner shipments also reached their lowest first-quarter volume in the last five years. Several factors may be contributing to this shift, including broader economic conditions, the refrigerant transition, and growing heat pump market share in new construction. But the longer-term direction remains clear: the market is continuing to move from air conditioners that only cool toward heat pumps that can both heat and cool.

Figure 2: In Q1, 2026, air conditioners and heat pump shipments were nearly at parity compared to the first quarter of previous years.

Heat pump growth is not limited to the United States. Preliminary data from the European Heat Pump Association shows that heat pump sales grew by 10.3% across 16 European countries in 2025, following a difficult 2024 when sales in 19 European countries fell 22% from 2023 levels. That rebound suggests renewed market momentum, though European sales remain uneven across countries.

This early 2026 shipment data points to a heating market in transition. Fossil fuel furnaces remain a significant part of the market, and quarter-to-quarter shipment data can fluctuate. But heat pumps are beginning the year from a position of strength, continuing a longer-term shift toward equipment that can deliver efficient heating and cooling in the same system.

Electric Heating in New Construction

The share of electric heating in homes has grown steadily over the past 75 years. While electric heating does not exclude the potential for gas to be connected to a building, it is far less common for a new building to be constructed with a gas line that isn’t also used for heating. Based on historical trends found in the Residential Energy Consumption Survey (RECS), homes with electric space heating also have electric water heating 86% of the time while homes with electric space heating (e.g. a heat pump) have a gas water heater only 14% of the time. Therefore looking at the share of electric heating in homes serves as a useful proxy for all-electric construction in the absence of data that isolates this subset.

In the 1950’s, electric heating served less than 1% of households as a primary heating source (Census). By 1970 that number had grown to 8%, then 26% in 1990 and then 41.3% in 2024 (Census). A recent study attributes this growth largely to U.S. electric prices compared to gas and heating oil, though there were certainly other factors at play. It notes that, from 1950 to 2020, “Average U.S. residential electricity prices have fallen 59% in real terms…while average residential prices for natural gas and heating oil have increased 22% and 41%, respectively.” While the natural gas industry has worked hard to cultivate a reputation as the “cheap” heating source, the market-driven shift toward electrification demonstrated below tells a different story.

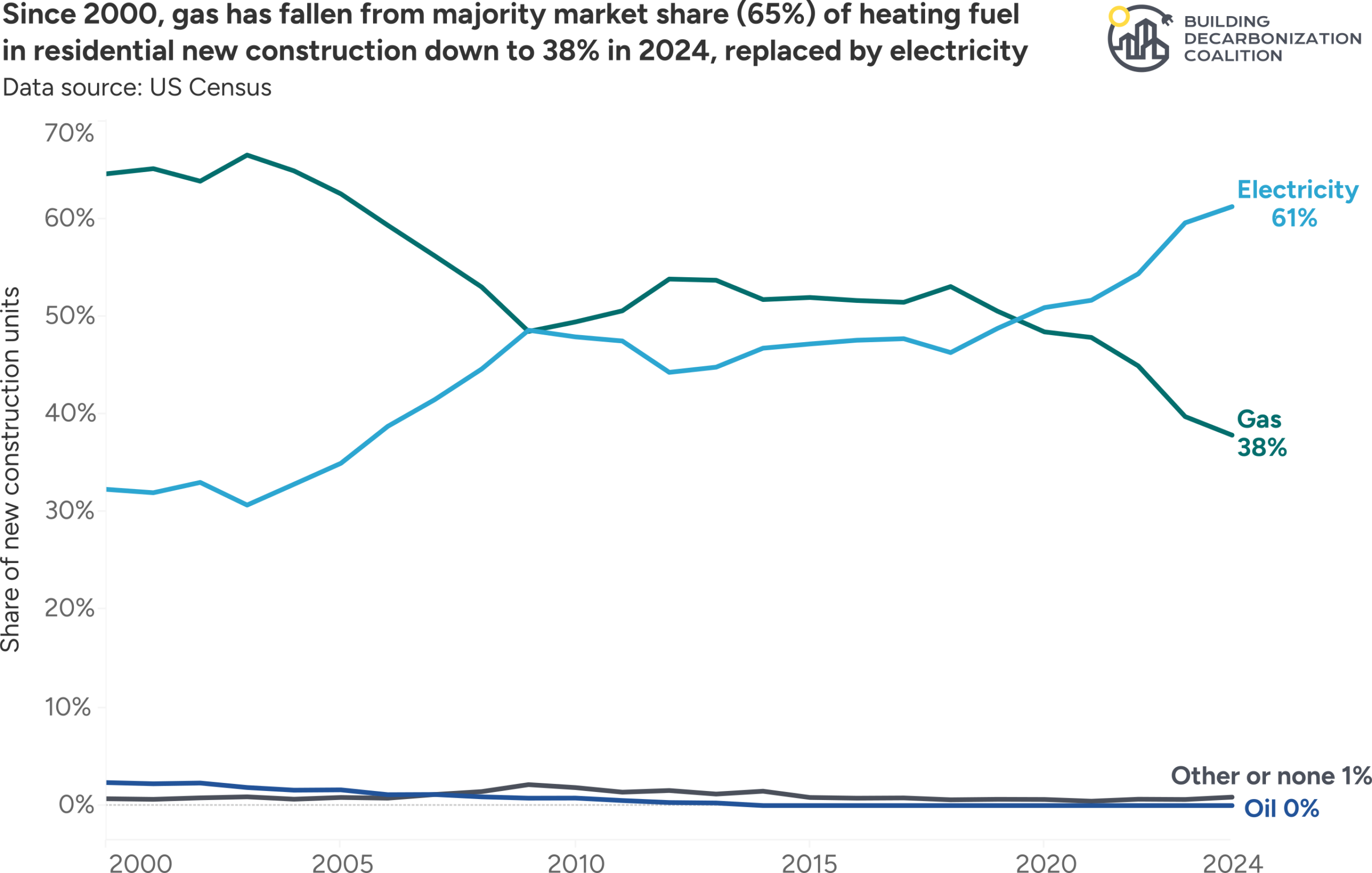

When we look at the market share of gas vs. electric heating in residential new construction, the momentum of electrification is clear. In 2000, gas heated roughly 65% of new housing units. By 2024, that share had fallen to 38%, replaced largely by electricity. Electric heating surpassed gas in new construction in 2020 and has continued to gain market share since.

Figure 3: Since 2000, gas has fallen from majority market share of heating fuel in residential new construction, supplanted by electricity. In this chart, “electricity” includes all electric heating types, including heat pumps, electric baseboards, and electric furnaces. “Gas” includes all gas heating system types, including furnaces and boilers.

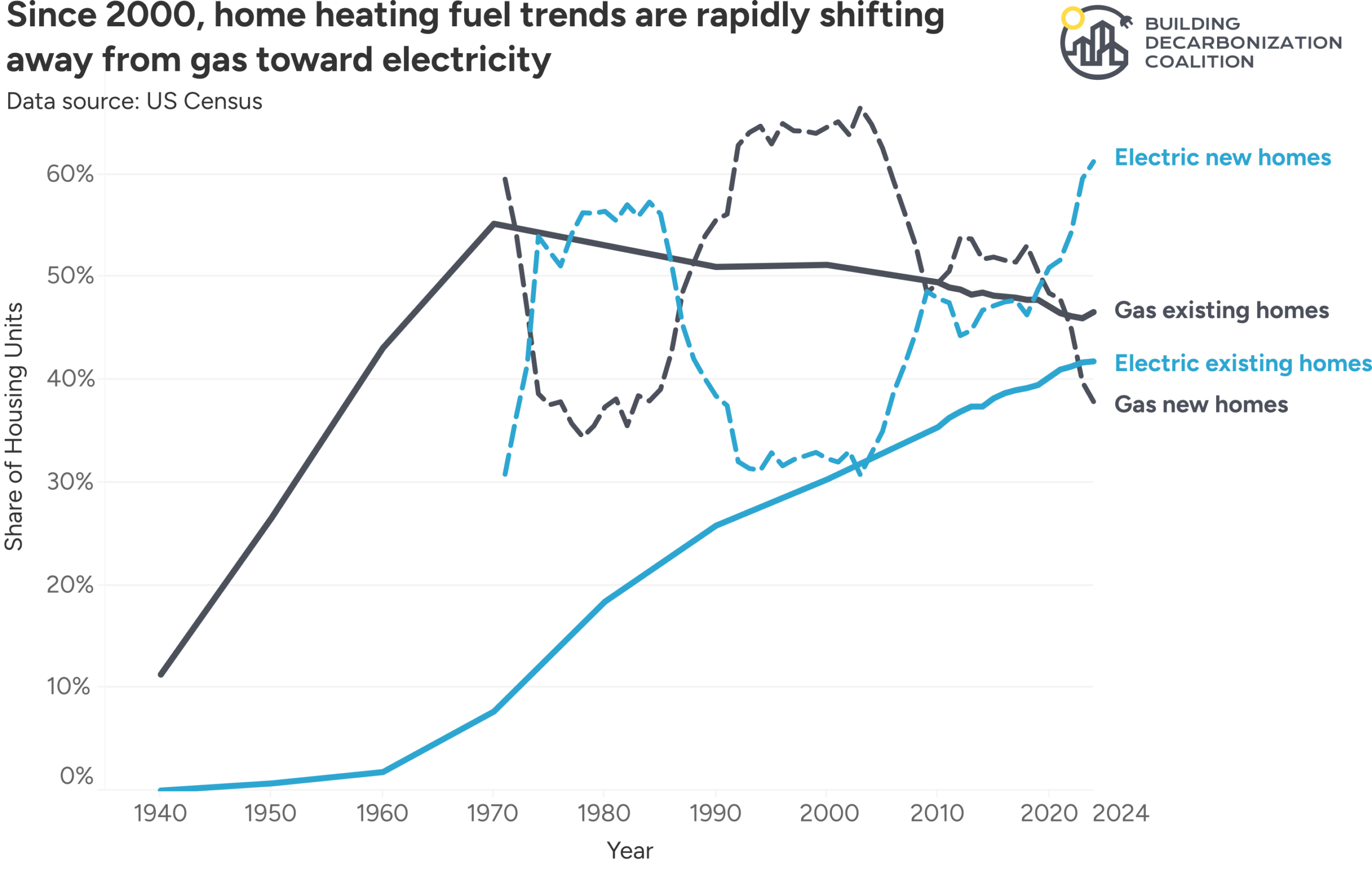

When new construction vs. existing buildings by heating fuel is viewed across a longer historical arc, the trend is even more stark, and demonstrates the effects of new construction on the continuing upward trajectory of all-electric homes vs. gas homes. In fact, the surge in (primarily) electric new construction has reached its highest point yet. The last time we saw a similar surge in the 1970s and 80s led to a significant increase in electric homes: an 18% increase over the course of those two decades. KB Home builders, one of the largest home builders in the U.S., demonstrates this growth in real time, as it has increased its all-electric home building by 18 percentage points 4 years. In 2021, KB homes built 30% of its homes as all-electric and in 2025 that figure had risen to 48%: nearly half of the homes.

Figure 4: Electric and gas heating trends in new vs. existing construction.

Another way to look at electrification growth in new construction is based on the primary equipment used for heating. The chart below shows that heat pumps are now close to becoming the leading primary heating system in new homes. In 2024, 46% of new housing units were installed with a heat pump, nearly matching forced-air furnaces at 47%. The remaining units were heated by hot water or steam systems, other systems, or no heating system at all. Because “forced-air furnace” can include both gas and electric systems, this chart should not be read as an exact one-to-one comparison between heat pumps and fossil fuel forced-air furnaces. But it does show how quickly heat pumps have moved toward the center of the new construction market.

Figure 5: Nearly half of new housing units are now installed with a heat pump. In 2024, forced-air furnaces accounted for 47% of new housing units, while heat pumps accounted for 46%.

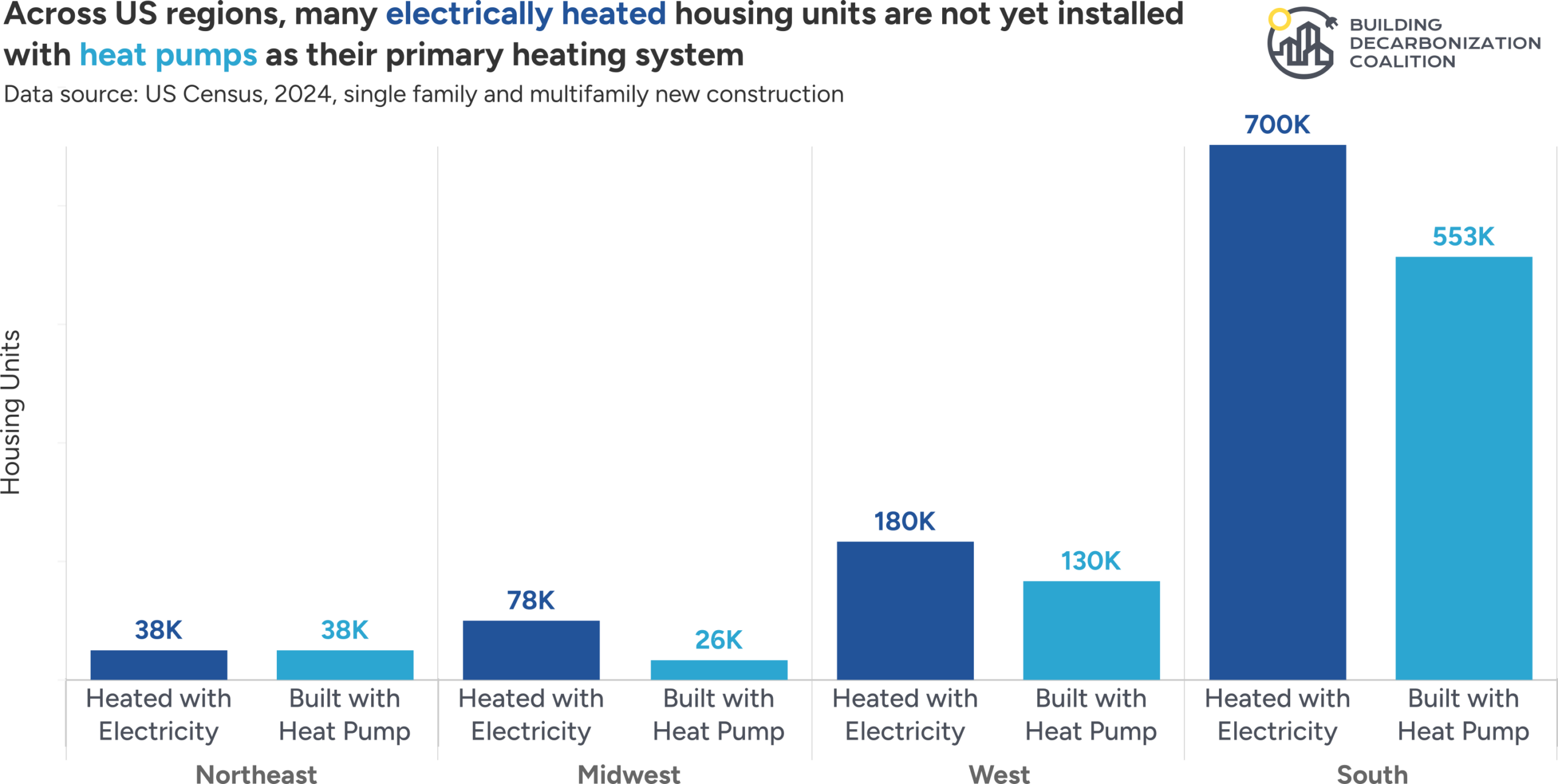

The regional picture of electric heating with heat pumps, however, is much more uneven. The South has historically led the country in heat pump adoption, and heat pumps remain most common there compared to other regions. But the Northeast and West are now seeing strong growth as heat pump technology improves, policy support expands, and new construction practices shift. The Midwest remains the lowest-adoption region for heat pumps in new construction, with heat pumps serving only 12% of new homes. There, electric heating has grown to roughly one in three new homes, suggesting that electric resistance heating may be filling part of the gap.

Figure 6: Across U.S. regions, many electrically heated housing units are not yet installed with heat pumps as their primary heating system.

The distinction between electric homes built with heat pumps and electric homes built with electric-resistance really matters, as electrification is not automatically the same as efficient electrification. A home heated with electric baseboards or an electric furnace may avoid on-site fossil fuel combustion, but it can still use far more electricity than a comparable home heated with a heat pump. Nationally, 75% of new electrically heated housing units in 2024 were installed with a heat pump, meaning one-quarter of electrically heated new homes still used another primary electric heating system. Across all new housing units, regardless of fuel, 46% were installed with heat pumps.

The electric resistance gap is one of the clearest remaining opportunities for improving affordability and reducing grid strain. Modern heat pumps are much more efficient than electric resistance heating, which means they can reduce household energy use while also lowering peak demand. RMI’s recent analysis finds that upgrading homes with electric resistance space and water heating to heat pumps can deliver substantial bill savings, reduce peak electric demand, and cut carbon pollution. They found that single-family electric-resistance households could save an average of $1,530 per year by upgrading electric-resistance space and water heating to heat pumps. For new construction, the implication is straightforward: the lowest-cost moment to avoid inefficient electric resistance heating is when the home is first built.

The momentum of electric heating, heat pumps, and all-electric homes reflects several overlapping changes in the building market: stronger energy codes, state and local policy, reform of gas line extension allowances, and continued innovation in the heat pump market, including cold-climate heat pumps, higher-efficiency equipment, and easier-to-install models, like 120V heat pump water heaters. It also reflects the economics of new construction: building all-electric from the start avoids the extra cost of extending gas service to a new home, while high-efficiency heat pumps for space and water heating can reduce long-term operating costs compared with less efficient electric resistance equipment or fossil fuel systems.

The Thermal Workforce

Heat pumps on their own cannot transform the market. A managed gas transition requires a diverse and skilled labor force. We use the term thermal workforce to describe the full spectrum of workers who deliver heating and cooling to buildings across fossil fuel and clean energy systems, rather than dividing this workforce into “fossil fuel” and “clean energy” categories.

The thermal workforce includes gas utility workers, pipeline and utility construction crews, and drillers, alongside electricians, plumbers, HVAC technicians, insulators, and other building energy professionals. It spans union and non-union labor, large utilities and small contractors, and urban and rural communities. Importantly, it reflects the reality that the transition from fossil fuel heat to clean heat will occur over decades and will require workers who can operate across systems during the transition period.

Recent data shows that the future of the workforce is particularly strong in the HVAC sector, with an uptick in enrollment for HVAC programs at two-year colleges: up 17% this spring compared to last spring and up 64% over the last five years. According to HomePros, “The enrollment surge reflects the growing interest in skilled trade jobs across the U.S., particularly among Gen Zers seeking alternative routes to stable, well-paying careers, as AI anxiety hangs over the white-collar workforce.”

III. Neighborhood Scale

Scaling up building decarbonization, block by block

Our neighborhood-scale project map is tracking 144 projects across North America, ranging from fully decarbonized neighborhoods to early plans to transition from fossil fuels. This crowdsourced map is constantly being updated with new projects and we need your help to keep it current. Please submit neighborhood-scale projects for consideration here.

Not included: It does not include all-electric neighborhoods that did not transition away from fossil fuels, or that are within communities with zero-emissions building standards. To learn where local and state governments are encouraging and requiring all-electric buildings, please visit our Zero Emissions Building Ordinance Tracker!

Project Highlight: Hayden, CO

Hayden, Colorado, shows how neighborhood-scale decarbonization can support economic transition in a fossil fuel-dependent community. After the planned closure of the Hayden coal plant, town leaders turned to a new business district as a long-term redevelopment strategy and chose a municipally owned geothermal thermal energy network to serve it. The project will anchor the 25-acre Northwest Colorado Business District, a greenfield development planned for roughly 230,000 square feet across 17 buildings. What makes Hayden especially noteworthy is that the system is being developed as a public thermal utility, giving the town a way to pair decarbonization with local control, predictable cost recovery, and long-term economic resilience.

Project details:

- 25-acre business district planned around a shared geothermal network

- Roughly 230,000 square feet and 17 buildings at full buildout

- Municipally owned thermal utility operated through a General Improvement District

- Phase 1 complete; Phase 2 underway, including a connection to Yampa Valley Regional Airport

- 560 tons of heating and cooling capacity planned at full buildout

- Around 130 boreholes, each roughly 1,000 feet deep

- Full elimination of on-site fossil fuels for heating

- Estimated annual emissions reduction of 1,498 metric tons of CO₂e

- $14 million total projected network cost at full buildout

- First-year operating savings projected at $15,900 compared to gas for a 7,000-square-foot office building

- Estimated geothermal premium of up to $100,000, with roughly seven-year payback before incentives

Above: A rig drills geothermal boreholes for the future thermal energy network in Hayden, CO. Photo Credit: Brooke Ashlee Photography.

Neighborhood-Scale Tools

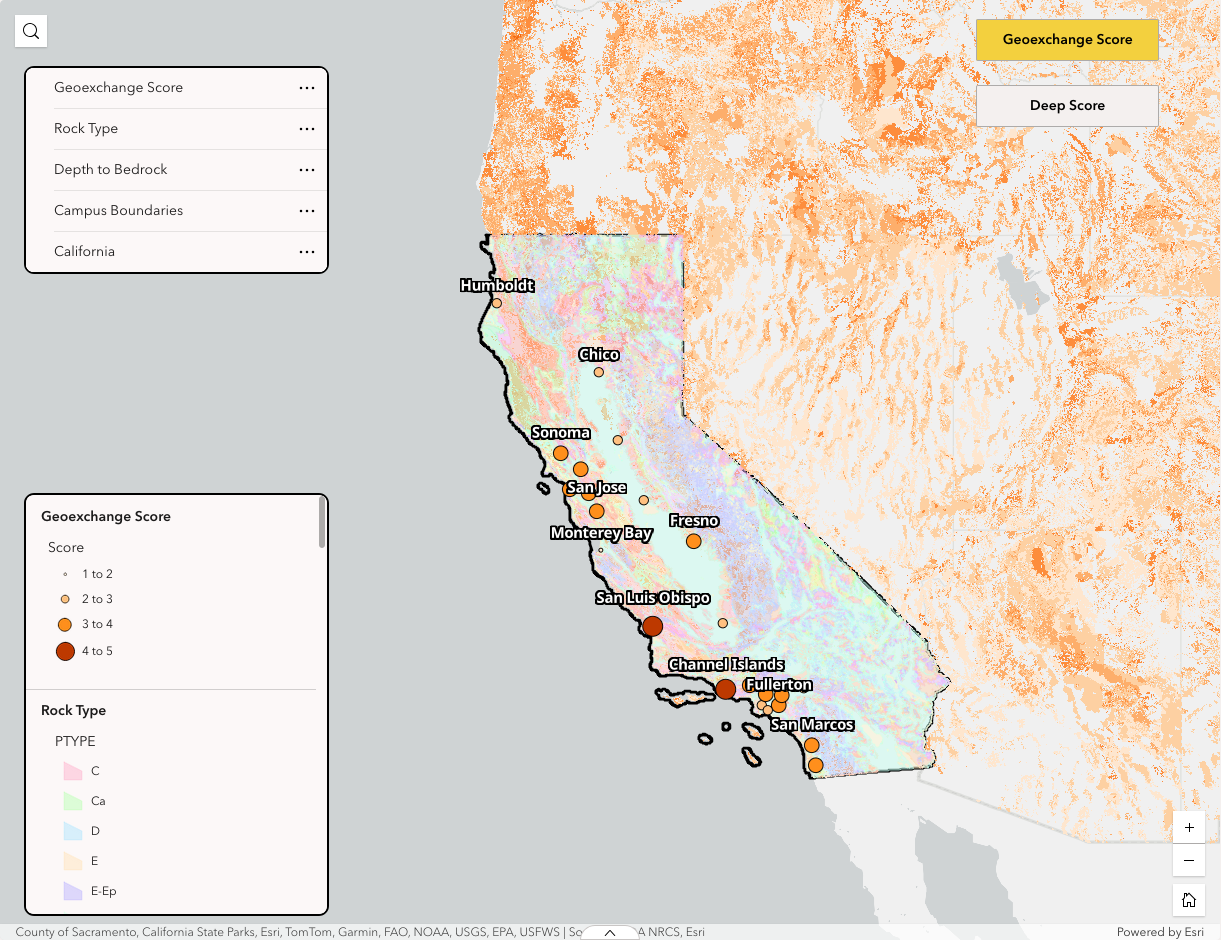

The California State University (CSU) Office of the Chancellor recently published a new tool for assessing the use of geothermal energy at each of the CSU campuses. The intention of the assessment is to support an initial comparative evaluation and prioritization and does not include site-specific feasibility, engineering design, or cost analysis.

The dashboard offers a geospatial representation of the study’s findings, and is divided into three categories: Infrastructure, Geothermal, and Enabling Conditions. It works by analyzing indicators such as bedrock depth, soil type, groundwater depth, and rock type and provides a ranking of the campuses based on their score. Based on these factors alone, CSU Channel Islands and San Luis Obispo are the top ranked sites for networked geothermal systems.

Explore the dashboard here: https://experience.arcgis.com/experience/40c55ea778e24a99a7a921f997cdd51f

IV. Gas System Costs and Affordability

How gas system spending is driving energy costs

Energy Affordability and Midterm Elections

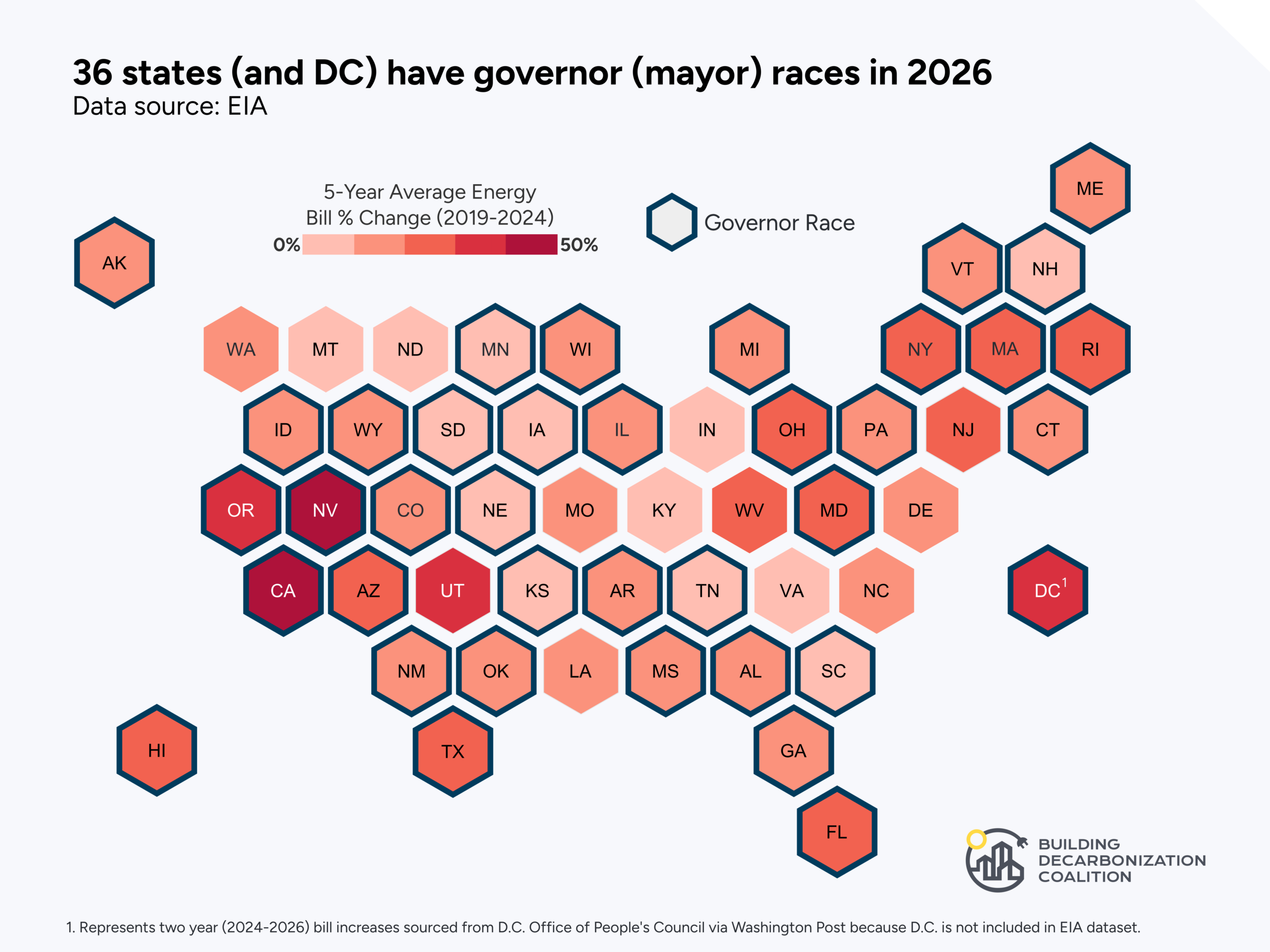

Figure 7: A map of 5-year average energy bill change (gas and electric) and states with gubernatorial races in 2026.

The map above shows where residential energy bills (both gas and electric) have risen most sharply over the past five years and where there will be gubernatorial elections this year. California has seen the highest rate increases–with a 49% surge in utility bills from 2019 to 2024, while Iowa has seen the least–with less than a 1% increase. In between, several states hover around a median increase of 17%. Meanwhile, there are over $16B in requested rate increases on the table across these states. With so many states grappling with rising energy costs, it is not surprising that we have seen this issue permeating midterm elections.

In the discussion below, we analyze how the campaign discourse in many of the 36 gubernatorial races and 22 public utility commissioner seats are representing the stakes of rising utility bills, energy costs, and rates, demonstrating how energy affordability has moved from a niche issue of utility regulation to become a broader voter issue. As a whole, this quantitative and qualitative data demonstrates how and where energy affordability has become both an economic and political pressure point.

Table of Midterm Races, Rate Cases, and Bill Increases

*South Carolina’s Commissioner seats were voted on by the General Assembly

How Energy Bills Are Shaping Midterms

Recent polling helps explain why utility bills are beginning to resonate as a political issue. In early 2026 and late 2025, polling found that “utility bills have joined groceries as a top tier issue in the affordability crisis,” with 78% of respondents reporting that their gas and electric bills had increased in the last year (Climate Power). Another poll found that 80% of respondents feel powerless to change or lower their energy bills, while a majority of Americans, 58%, “do not fully understand what drives their monthly energy bills” (Powerlines-Ipsos).

That frustration is increasingly showing up in politics. While political campaigns are not polls, they do offer a revealing signal about what politicians believe voters are worried about, often based on polling and message testing campaigns have conducted themselves. Candidates spend time on the issues they think will resonate with voters, and this year, utility bills are increasingly being treated as part of the broader affordability crisis. Against a backdrop of gas and electric utilities seeking billions more from ratepayers through new rate cases, energy costs are now appearing in campaign debates over cost of living, corporate accountability, climate policy, and AI-fueled data centers.

The campaign language itself reflects the same sense of confusion and powerlessness captured in the polling. In Arizona, Corporation Commission candidate Clara Pratte argued that “it shouldn’t take a rocket science degree” for customers “to figure out how to manage your utility bills” (Cronkite News). And in D.C., where gas and electric bills have become a major issue in the Democratic mayoral primary, The Washington Post observed that “utility bills are not typically the stuff of brass-knuckle politics,” but that the “soaring expense of gas and electricity bills” has “lit a fuse” in the campaign there. That primary has since concluded, with Janeese Lewis George winning the Democratic nomination after a campaign centered in part on affordability and utility accountability (Washington Post).

But candidates aren’t simply saying that bills are too high. They’re using utility bills to make arguments about regulation, corporate accountability, public oversight, and cost allocation. Across key states where rising bills, pending rate cases, gubernatorial races, and public utility commission elections are converging, four themes have emerged:

- Utility bills are turning regulation into a voter issue. Across states, candidates are not only acknowledging that energy costs are high, but pointing voters toward the utility commissions, regulators, and investor-owned utilities that shape those costs. This is especially visible in states with public utility commission elections, where candidates are making the once-obscure work of utility regulation part of the campaign itself. In Arizona, Corporation Commission candidate Clara Pratte warned that “if we don’t elect new leaders to the Arizona Corporation Commission, our bills are going to keep having some of the highest rate increases in the country” (Cronkite News). The same message is also showing up in gubernatorial races. In Wisconsin, Democratic gubernatorial candidate Mandela Barnes pledged: “As Governor, I will freeze utility rates and take on monopolies like WE Energies who are exploiting ratepayers to line their own pockets” (State Affairs), framing utility affordability as something elected officials can change if the political will is there, and that high rates are not merely something households must absorb. And in Michigan, Democratic gubernatorial candidate Jocelyn Benson connected affordability to regulatory transparency and reform, saying, “No more conflicts of interest on the MPSC board. No more closed-door rate decisions. And no more guaranteed profits before a single dollar goes to fixing the grid” (Michigan Public). These messages suggest that candidates believe voters are increasingly receptive to seeing utility bills not just as individual household expenses, but as regulated costs shaped by decisions that can be challenged, scrutinized, and reformed.

- Rate cases are becoming campaign flashpoints. As utilities seek approval for new rate increases, candidates and public officials are using these proceedings to question whether proposed costs are justified and whether regulators are doing enough to protect ratepayers. In Pennsylvania, Governor Josh Shapiro put a spotlight on PECO’s now-withdrawn proposed rate hike, characterizing it as “pure greed” and saying, “I’ll do everything I can to stop it” (WHYY). He also argued that the utility “made an obscene $814 million in profit” and “could have used that money to offset people’s costs,” but instead “passed it onto shareholders” (WHYY). In Alabama, Public Service Commission candidates have made a similar case for opening up the rate-setting process, with Sheila McNeil arguing, “I think the first thing that is important is that we open up the books and do a rate case review” (Alabama Reflector). In Georgia, PSC candidate Peter Hubbard described the commission’s role as “acting as a shield to imprudent spending” and argued that a proactive commissioner can identify lower-cost solutions (The Current/WABE). And in Connecticut, candidates are using Eversource’s planned rate increase as a reason to question whether regulators are doing enough to protect customers. Governor Ned Lamont said PURA should take “a good, hard look” at the request and “protect our consumers,” while Democratic challenger Josh Elliott called for revoking Eversource’s exclusive franchise so municipal utilities and a public option could become “real choices” (WSHU). Lamont has since proposed a broader utility accountability package that would require utilities to periodically earn renewal of their monopoly franchise, expand subpoena power for the Office of Consumer Counsel, and add cost-effectiveness and affordability analysis to utility oversight (CT Mirror). This messaging frames elected officials and utility regulators as ratepayer protectors who can intervene and shield customers from unnecessary rate hikes.

- Candidates are competing to define what’s causing bill increases. Utility bills bundle together many different cost drivers, including fuel prices, infrastructure spending, taxes, disaster recovery, and utility profits. Because those drivers are not always clearly delineated, candidates have room to tell very different stories about why bills are rising. In California’s gubernatorial primary, candidates from opposite sides of the aisle agree on one culprit while differing on others in this multilayered problem. Former Democratic candidate Tom Steyer and Republican nominee Steve Hilton both point to utility monopoly power as a main driver of higher bills, though they differ on the path forward. Steyer argues that “we have to take on these electric monopolies” and that breaking up “monopolistic power utilities” would drive down costs (CalMatters), while Hilton pairs his critique of monopoly power with an attack on the state’s climate policies and renewable energy standards (Hilton Campaign). By comparison, Becerra has framed rising bills less around a single culprit than around affordability, oversight, and accountability, arguing that the clean energy transition cannot come at the cost of higher bills for low-income families and that “we also need stronger oversight and accountability of our utilities” (Becerra Campaign). Now that the race has narrowed to Xavier Becerra and Hilton, the general-election debate is likely to continue centering on affordability, oversight, accountability, and competing explanations for why utility bills are rising. In New York, Governor Kathy Hochul has pointed to the need for utility accountability to lower bills, saying she is “laser-focused on energy affordability and reliability” while “holding utility companies accountable to protect consumers from unfair practices” (New York Governor’s Office). Similar to Hilton in California, New York’s Republican gubernatorial candidate Bruce Blakeman has tied rising utility costs to the state’s clean energy agenda, calling the state climate law a “utility bill bomb that is exploding on kitchen tables across New York” (South Shore Press). Blakeman has continued to make energy affordability a core campaign theme, including by promising to cut utility bills by ending New York’s fracking ban and expanding oil and gas production (Wellsville Sun). The result is a campaign debate in which the same monthly bill becomes evidence for very different agendas: breaking up utility monopolies, strengthening oversight, freezing or investigating rates, expanding energy supply, or rolling back climate and energy policies.

However these explanations still leave out one major structural cost driver: long-term gas-system spending. BDC’s own research has shown that, for many gas customers, more than two-thirds of the bill now goes toward maintaining and expanding the gas system, while roughly one-third pays for the gas itself. And yet this structural cost driver has not surfaced as prominently in political messaging as utility profits, climate policy, or data centers.

- Candidates are framing rising utility bills as a matter of ratepayers versus corporations. In Michigan and Ohio, candidates are using data centers to ask whether households and small businesses should pay for grid upgrades and energy demand created by large corporate customers. In Ohio, Democratic gubernatorial candidate Amy Acton makes this cost-shifting frame explicit, writing that “new data centers are causing bills to increase” and pledging to ensure that “Ohio consumers and other ratepayers are not the ones shouldering these added costs” (Amy Acton campaign). In Michigan, Benson’s energy plan similarly includes a promise to “ensure corporations—not ratepayers—pay the cost of increased energy demands” (Michigan Public). Commission races are homing in on this issue, too. In Georgia, Public Service Commission candidates across parties are debating whether ordinary customers should pay for infrastructure built to serve data centers. During the Republican PSC primary, Bobby Mehan argued that the commission should consider “clawing back” billions authorized for plants that will serve large users, “particularly data centers”; although Mehan did not advance to the general election, the debate shows how data-center cost allocation has become a campaign issue in utility-regulator races (Georgia Public Broadcasting). In other states, the utility as a corporate actor is at the center of the debate. In California, for example, wildfire cost recovery raises a parallel question about whether customers should bear the rising costs of climate risk, grid hardening, and utility liability, or whether utilities and shareholders should absorb more of the costs associated with their own infrastructure and risk management decisions.

Whether or not these candidates are successful at the polls, the widespread attention to energy costs beyond the price of gasoline reveals a growing anxiety, awareness, and concern around how utility costs are allocated, who gets to make decisions about rates, and what is causing energy bills to continue to rise at a rate that outpaces inflation.

V. The Thermal Transition

Empowering communities, transitioning workers, and achieving our climate goals through clean energy infrastructure

The thermal transition is the long-term evolution of the thermal sector toward cleaner, more affordable, and more efficient ways of delivering heating and cooling. It offers an inclusive framework for understanding the future of heat: a shift away from the legacy fuels and systems that once defined the heating industry and toward modern solutions that support cleaner air, healthier communities, and lower energy bills.

In this section, we track the legislation and regulatory proceedings helping manage the transition from the gas system to clean thermal infrastructure, including electrification and thermal energy networks.

2026 Legislation: Affordability Focus

As energy bills continue to strain households, state legislatures are advancing bills that treat affordability as both an immediate consumer protection issue and a long-term energy planning challenge. Below we highlight 22 building decarbonization bills across 12 states that address the expansion of low-income assistance, improved access to weatherization and heat pumps, limiting certain utility costs charged to ratepayers, and strengthening protections against shutoffs. As of mid-June, 10 of these bills have passed, 6 remain in progress, and 6 have failed or were held during session. These bills show that states are using affordability policy to address both monthly bill pressure and the underlying systems that determine how energy costs are distributed.

Energy Affordability and Decarbonization Bills

|

State / Bill |

Description |

Categories |

|

California, Residential Heat Pump Systems (SB 222) 🟡 In Progress |

Standardizes the heat pump permitting process by creating a pathway for automated permitting, requiring fee transparency, establishing guardrails on setback and noise limits, and prohibiting HOAs from banning heat pumps. |

Consumer Protections |

|

California, Gas Corporations: Gas Distribution Service Line Replacements: Alternatives (AB 2313) 🟡 In Progress |

Requires gas utilities to offer customers the choice of an incentive in lieu of replacing an old gas service line planned for replacement. The proposed incentive would be capped to ensure that some of the planned pipeline replacement work would be avoided, ensuring a lower overall cost to ratepayers. |

Affordability |

|

California, Natural Gas Ratepayer Protection Act (SB 1359) 🟡 In Progress |

Requires gas companies to report costs associated with gas infrastructure replacement to the commission and before authorizing cost recovery, the commission shall consider whether cost-effective alternatives such as electrification and nonpipeline alternatives could reasonably avoid or reduce those costs. |

Consumer Protections |

|

Illinois, POWER Act (SB4016/HB5513) 🔴 Held |

Establishes guardrails for hyperscale data centers including: ensuring infrastructure costs are not shifted to consumers, creating clear standards for interconnection and cost recovery, aligning new demand with clean energy supply, and establishing critical protections to limit pollution and sustainable water use. The POWER Act did not pass during the regular session, but is expected to be taken up during the veto session later this year. |

Consumer Protections |

|

Indiana, Electric Utility Affordability (HB 1002) 🟢 Passed |

Implements a series of policies to address affordability, including assistance for low-income qualified households and a summer disconnection moratorium for low-income qualified households. |

Consumer Protections |

|

Indiana, Various Utility Matters (HB1111) 🔴 Failed |

Would have provided more protections against disconnections, including prohibiting a reconnection charge, implementing a summer disconnection moratorium for eligible households. |

Consumer Protections |

|

Kentucky, An Act Relating to Utility Disconnection Protections (HB377) 🔴 Held |

Would have prohibited winter and summer disconnections when temperatures exceeded a certain limit, establish a certificate of need for households at risk, and limit the days in which disconnections could occur. |

Consumer Protections |

|

Maryland, Investor-Owned Electric, Gas, and Gas and Electric Companies – Cost Recovery – Limitations (HB0001) 🔴 Held |

Would have prohibited BGE and other investor-owned utilities from passing along the high costs of executive salaries to Maryland ratepayers. The bill would also add new restrictions on charging customers for events and advertising. |

Consumer Protections |

|

Maryland, Utility RELIEF (Reducing Energy Load Inflation for Everyday Families) Act (HB1532/SB841) 🟢 Passed |

The Utility RELIEF Act includes building decarbonization provisions that will help lower Marylanders’ energy bills and create jobs by encouraging the adoption of heat pumps, which efficiently deliver both heating and cooling from a single appliance. These provisions include: – An allocation of $72.65 million in funding to Maryland’s Residential Energy Equity Program, which will help low- and moderate-income households install modern, efficient, zero-emission heat pumps. – An update to the state’s Strategic Energy Investment Fund (SEIF) authorizing it to fund loan, grant, rebate, and other incentive programs that support the electrification of Marylanders’ buildings and transportation. – Direction to the Maryland Energy Administration to develop programs that can provide grants and loans to businesses and homeowners seeking to weatherize, install heat pumps, or otherwise upgrade their buildings to achieve Maryland’s Building Energy Performance standards. The Utility RELIEF Act also includes provisions regarding utility ratemaking, data center tariffs and registry, creation of a reverse auction to encourage new clean energy generation, and changes to Maryland’s energy efficiency programs. |

Affordability |

|

Massachusetts, An Act Relative to Energy Affordability, Clean Power, and Economic Competitiveness (H5151) 🟡In progress |

This bill aims to reduce energy burdens on Massachusetts ratepayers, though the approach from the House and Senate diverges. For the House bill, according to the Environmental League of Massachusetts, “the bill removed threats to our Commonwealth’s net-zero climate goals, does not require an affordability test for climate programs, and no longer puts the burden of paying for gas pipelines on electric customers. While this bill makes meaningful progress, it also proposes cutting $1 billion in funding for Mass Save, which would effectively decimate one of the Commonwealth’s most effective tools for lowering energy bills.” On the other hand, on June 24th, the Senate released its version of the bill that did not include cuts to Mass Save, but would establish more oversight and limit overhead spending for the program. The Senate frames the bill as a hunt for ‘pockets of overspending and overcharging that in some cases are legacies of past policies that have exhausted their usefulness’ within utilities” and notably include the phasing out of the GSEP program (ABC 10 Boston). The house and senate will ultimately negotiate to align the two approaches. |

Affordability |

|

Minnesota, Commission to Promote Affordable Service and Consider Customers’ Ability to Pay Rates Requirement (SF3992/HF3777) 🔴Held |

Would have amended Minnesota’s statute to include that when the commission is determining whether utility returns are fair and reasonable, it must consider customers’ ability to pay the rates used to fund the return on equity. |

Affordability |

|

New York, Prohibits Termination of Electricity or Heat Services During Forecasts of Extreme Temperatures (S120A) 🟢 Passed, awaiting governor’s signature |

Reintroduced from 2025. Prohibits the disconnection of electricity or heat services during extreme weather. |

Consumer Protections |

|

Pennsylvania, An Act Amending Title 66 in Rates and Distribution System, Providing for Return on Equity (HB 2224) 🟡In progress |

This bill “would cap the return on equity (ROE) that investor-owned utilities can earn during rate cases…It establishes a formula-based cap tying the default authorized ROE to the 10-year U.S. Treasury bond yield plus two percentage points. It also creates a competitive equity auction process for utilities that challenge the formula, ensuring any approved return reflects actual market conditions.” (Evergreen Action). |

Affordability |

|

Pennsylvania, An Act Amending Title 66 (HB 2333/SB154) 🟡In progress |

This bill would reinstate Chapter 14, which establishes consumer protections against disconnections. This bill also amends Chapter 14 to include more protections and extends the sunset date of this Chapter to 2036. |

Consumer Protections |

|

South Carolina, Utility Billing Accountability and Consumer Protection Act (H5282) 🔴 Held |

Would have established a series of transparency measures, including PSC approval for billing changes, 90-day advance customer notice, and require utilities to implement consumer protections for rural energy-burdened households. |

Consumer Protections |

|

Virginia, Electric Utilities; Energy Efficiency Upgrades, Report (HB2/SB72) 🟢 Passed |

This bill will lower low-income energy bills and related air pollution by requiring that utilities create a program to shift low-income customers still stuck on old oil or propane heat over to high-efficiency, lower-polluting electric heat pumps. |

Affordability |

|

Virginia, Income-Qualified Energy Efficiency and Weatherization Task Force, Established, Report (HB3/SB5) 🟢 Passed |

Establishes the Income-Qualified Energy Efficiency and Weatherization Task Force to improve coordination across utilities, state agencies, and federal, municipal, and private funding sources to more effectively deliver energy efficiency, weatherization, and weatherization-ready repairs for income-qualified Virginians. |

Affordability |

|

Virginia, Electric Utilities; Percentage of Income Payment Program, Eligibility, Delayed Effective Date (HB884) 🟢 Passed |

Simplifies the process for accessing the Percentage of Income Payment Program (PIPP), allowing for more households to apply. |

Affordability |

|

Virginia, Utilities, Certain; Notice Procedures for Nonpayment (HB1002) 🟢 Passed |

Requires utilities to make reasonable efforts to work with customers before disconnection. |

Consumer Protections |

|

Virginia, Electric Utilities; Pilot Programs for Energy Assistance and Weatherization for Certain Individuals (SB253) 🟢 Passed |

Extends the sunset date of the annual pilot program conducted by Dominion Energy Virginia and Appalachian Power Company for energy assistance and weatherization for low-income, elderly, and disabled individuals from 2028 to 2038, “directs the SCC to ensure that residential customers do not pay electricity generation and distribution costs to serve data centers”, and reduces regulatory oversight for Dominion’s undergrounding program (Inside Climate News).

Advocates are concerned about the cost impacts on ratepayers given the reduced regulatory oversight of Dominion’s Strategic Underground Program (SUP). |

Consumer Protections |

|

Washington, Protecting Tenants from Periods of Extreme Heat (HB2265/SB6200) 🟢 Passed |

This bill affirms tenants’ right to install and use portable cooling devices (Shift Zero). |

Consumer Protections |

|

Washington, Authorizing Community Scaled Weatherization Projects (HB2338/SB6223) 🟢 Passed |

According to Shift Zero, “HB 2338 allows agencies that lead weatherization projects to carry out larger, community-scale projects that serve multiple homes and/or apartments under the umbrella of one larger project. This will simplify management, help attract contractors to rural areas in cases where travel costs would be prohibitive for smaller-scale projects, and allow weatherizing agencies to reach more homes faster and at lower cost.” |

Affordability |

Line Extension Allowance Reform: 2026 Update

Previously a banal cost-shifting mechanism, gas line extension allowances (LEAs) have become controversial policies that are stirring up debate across the U.S. as more states move to remove this unfair gas system incentive.

When we did a deep dive into the state of play for LEAs last year, we found that utility customers across the United States could save up to $7 billion annually if policymakers reformed gas line extension allowances (LEAs) in every state. LEAs are incentives for new customers to join the gas system that are paid for by existing customers. While the amount of the incentive varies widely (often in the thousands), studies continue to show that the justification for this incentive no longer pencils out as gas system growth slows and stagnates.

When we last checked in, we saw that six states have already made partial or full reform to these subsidies and six more states and D.C. are actively considering removing gas LEAs. Those numbers hold true today, though the activity within those in-progress states has picked up in recent months.

Figure 9: Line extension allowance reform activity

Q2 2026 LEA Reform Updates

|

State |

Status |

LEA Reform Updates |

|

California |

Passed |

California was the first state to eliminate LEAs in 2022 through regulation, and followed that decision in 2023 with eliminating electric LEAs for new construction mixed-fuel buildings. It is the only state to eliminate electric LEAs for new construction. Since 2023, line extension data collected by the California Public Utility Commission (CPUC) has seen steady gains in all-electric new construction rates (CPUC). In Q4 2025, all-electric new construction rates on the residential side were 73% for PG&E, 48% for SCE and 68% for SDG&E. For the non-residential side, all-electric new construction rates were 89% for PG&E, 76% for SCE, and 48% for SDG&E (CPUC). |

|

Colorado |

Passed / Litigation Pending |

Colorado eliminated LEAs in 2023 through legislation (SB23-291), however, in May 2026 Colorado Natural Gas Inc. (CNG) introduced a lawsuit challenging Colorado’s change to its LEA policy. CNG raised two main issues with the statute: 1) it argues that only service line allowances should be eliminated, as main lines and shared infrastructure are “essential to the overall utility system’s basic operation, and its associated costs reflect more than the cost of connecting one new customer” (16). 2) CNG claims that the statute itself violates federal and state Contract and Takings clauses and impairs the regulatory compact that allows CNG to earn a reasonable rate of return on its investments in exchange for the obligation to serve. Though SB23-291 is being challenged in the courts, Colorado’s original LEA policy was established by regulation, and did not strictly need legislative action to be revised. Furthermore, while SB23-291 eliminated the monetary incentives given to new gas customers and charged to existing customers, the option for customers to connect to the gas system has not been impacted. Rather, the true economic cost of connecting to the gas system has been revealed. |

|

D.C. |

In progress |

D.C. first began discussing the reform of gas LEAs in formal case #1167 via a straw proposal for a gas planning framework that included eliminating LEAs. Within FC#1167, the Public Service Commission (PSC) requested stakeholder comments on establishing a separate gas planning proceeding. In March 2026, with support from stakeholders, the PSC initiated FC#1187 (Order No. 22799), “In the matter of the investigation into the implementation of integrated natural gas distribution system planning,” and proposed to follow the Clean Energy Cohort Roadmap developed by the National Association of Regulatory Utility Commissioners (NARUC). Within the roadmap is a recommendation to review system costs that specifically identifies existing LEAs and whether they should be limited or eliminated. Currently, stakeholders are providing comments on the proposed roadmap. |

|

Illinois |

In progress |

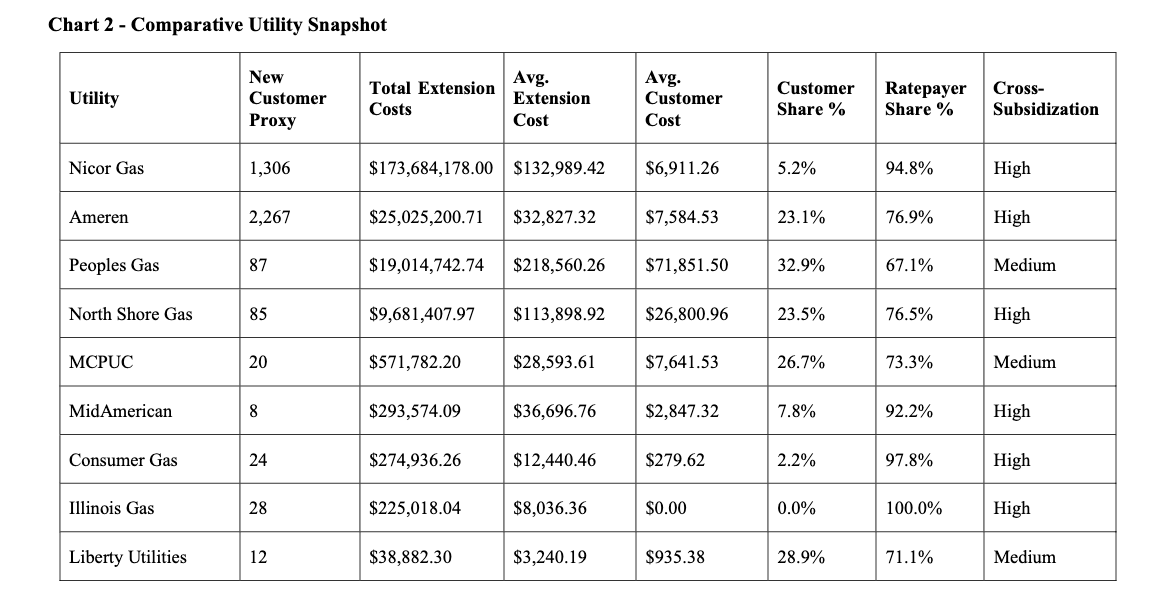

Gas LEAs remain under active review in IL. The ICC ordered a statewide study after finding that “the historic policy rationale for line extension allowances has changed,” with a final version submitted to the Commission in May 2026. (Illinois Commerce Commission). The study evaluated cost causation, equity, long-term gas demand, and stranded asset risk. It found that utilities use different models, including footage-based allowances, cost-equivalent approaches, revenue-screened approaches, and rider-centered approaches to calculating LEA amounts. Despite those differences, the report found a consistent outcome: existing ratepayers, not new connecting customers, bear most line-extension costs. Customer contributions ranged from 0% to roughly 33%, while ratepayer responsibility was the majority in all cases and exceeded 90% for several utilities. The range of line extension costs reported by the utilities also varied widely, as demonstrated in the chart featured below, ranging from $3K to $132K as the average line extension cost. Due to this high cost and disproportionate share between new customers and existing ratepayers, there is a very high degree of cross-subsidization across the majority of the utilities. The report concluded that Illinois’ current framework does not consistently align cost responsibility with cost causation and results in material cross-subsidization across customer groups. Rather than recommending an immediate end to gas line extensions, however, the report recommends a phased reform path focused on standardized reporting, clearer cost-allocation rules, customer-facing disclosure, minimum customer contribution thresholds, and better treatment of refunds and financial risk. |

|

Maine |

In progress |

In May 2025, Maine initiated its Future of Gas proceeding under Docket No. 2025-00145, “Inquiry Regarding Future of Natural Gas.” A major focus within the proceeding is to review gas infrastructure investments, including LEAs, and their climate impacts (Maine Future of Gas). |

|

Maryland |

In progress / Delayed |

Maryland moved toward eliminating gas LEAs through its Future of Gas proceeding, but this action has recently been delayed. The PSC found that the status quo for funding gas line extensions may no longer align with the state’s greenhouse gas reduction and electrification policies. In June 2025, the PSC ordered staff to draft regulations that would require new gas customers to pay the full upfront cost of extending service, rather than shifting those costs onto existing ratepayers. The Commission framed the change as a neutral cost-causation reform, not a restriction on customer choice: customers could still choose gas service, but without artificial subsidies. The PSC also emphasized stranded-cost risk, noting that new gas extensions may not be fully recovered through rates over the lifetime of the assets and that existing ratepayers should not be left responsible for those costs (Maryland Public Service Commission). |

|

Massachusetts |

In progress |

Massachusetts’ LEA deliberations remain active in the utility Climate Compliance Plan dockets. In D.P.U. 20-80-E, the Department proposed eliminating gas line extension allowances by requiring new gas customers to pay the full cost of their own gas connections, and clarified that final determinations would be made in the CCP dockets. The utilities filed revised tariffs and joint testimony on October 20, 2025, arguing that existing LEA/CIAC policies are not subsidies but revenue-based cost-allocation mechanisms, and that eliminating allowances would force new customers to pay twice, raise housing and development costs, create implementation problems, and potentially push some projects toward higher-emitting fuels where electrification is not feasible. Advocates, DOER, and consumer/environmental parties counter that LEAs socialize the risks of new gas infrastructure across existing ratepayers, rely on long-term gas demand assumptions inconsistent with the state’s 2050 climate mandate, and undermine the DPU’s Future of Gas framework by continuing to encourage gas-system expansion. Deliberations on the line extension allowance policy are continuing well into 2026. |

|

Minnesota |

In progress/ partial reform |

Advocates argue that ending LEAs could save customers an estimated $34 million each year. (Clean Heat Minnesota). Minnesota has now adopted a partial reform package for gas LEAs through its Future of Gas docket, though the official order is still forthcoming. At its June 4, 2026 hearing, the MPUC moved to cap free footage allowances at no more than 75 feet for service lines and 80 feet for mains (155 feet total), unless a utility justifies a different level in a rate case. For reference, existing allowances varied by utility: CenterPoint was listed at up to 175 feet combined main and service and Xcel was already limited up to 155 feet combined main and service. The Commission also prohibited additional residential contribution-in-aid-of- construction waivers (CIAC) beyond the standard allowance, while directing utilities to consult with the Attorney General on whether targeted waivers may be appropriate for customers who cannot afford upfront extension charges. Utilities must update tariffs, report CIAC waivers annually, survey new customers and builders about what heating systems they would have chosen if gas service were unavailable, and revisit LEA policies if gas throughput or average residential gas use declines for three consecutive years. The decision does not substantially lower the amount existing customers can be asked to subsidize but it raises the evidentiary bar for future allowances, and begins tying gas extension policy to declining gas demand, electrification, and stranded-asset risk. |

|

New Jersey |

In progress |

In March 2023, New Jersey initiated its future of gas proceeding, In the Matter of the Implementation of E.O. 317 Requiring the Development of Natural Gas Utility Plans (Docket # GO23020099) to align the state’s climate goals with utilities operations. Included within the docket was to consider the “elimination of subsidies that encourage unnecessary investment in natural gas infrastructure that is likely to result in stranded costs to customers” (Order). There has been no activity documented in the docket since July 2023. |

|

New York |

Passed / Pending Implementation |

Gas LEAs have been eliminated statewide for new residential gas hookups starting in December 2026. Gov. Hochul signed S.8417/A.8888 on Dec. 19, 2025, with a chapter amendment directing implementation in 1 year, ending the “100-foot rule” that required existing ratepayers to subsidize the first 100 feet of new gas lines. The PSC has proposed the revised language for Title 16 of the New York Code of Rules and Regulations Part 230 and solicited comments on the language. |

|

Oregon |

Passed / Phasing out |

Oregon has adopted utility-specific LEA reforms, with phaseouts underway for major gas utilities. Avista’s gas LEA are scheduled to reach $0 by January 2027 and NW Natural’s should reach $0 by November 2027. In its 2026 Integrated Resource Plan (IRP) review, Oregon PUC staff also directed NW Natural to explain how the LEA phaseout will be incorporated into its load forecasting and demand scenarios, making the reform part of longer-term gas planning (OPUC). |

|

Rhode Island |

In progress |

Gas LEAs are now a live policy issue in Rhode Island. Rhode Island Energy currently provides gas LEAs though reform is being considered through the state’s Future of Gas docket. In 2026, a Senate resolution requested that the Rhode Island PUC terminate gas LEAs as part of Rhode Island Energy’s rate case, Docket 25-45-GE, citing customer cost-shifting and the state’s emissions reduction requirements (Senate Resolution). On June 10, 2026, the Senate approved the resolution, urging the PUC to examine the impact of gas LEAs and determine whether they should be allowed to continue. |

|

Washington |

Passed/ Phasing out |

Like Oregon, Washington has adopted utility-specific LEA reforms, with phaseouts complete in January 2025 for Avista and Puget Sound Energy and with Cascade Natural Gas phasing out by March 2027. NW Natural is the remaining large gas utility in Washington that still offers gas LEAs without a phaseout date. |

Figure 10: From Illinois Commerce Commission’s recently released report on line extension allowances, showing that average gas LEAs range from $3-132K, with most of the cost burden carried by existing customers (“ratepayers”), resulting in high cross-subsidization—a phenomenon that public utility commissions want to avoid (pg. 73).

Future of Gas

The “Future of Gas” is an evolving policy framework used to describe the questions, assumptions, and arguments surrounding the long-term sustainability of the methane gas system. Researchers, state energy offices, legislators, and utility regulators have used the phrase to describe policies, reports, and proceedings since at least 2019. Advocates have also applied it retroactively to highlight the growing number of regulators and legislators critically examining the gas system’s longevity.

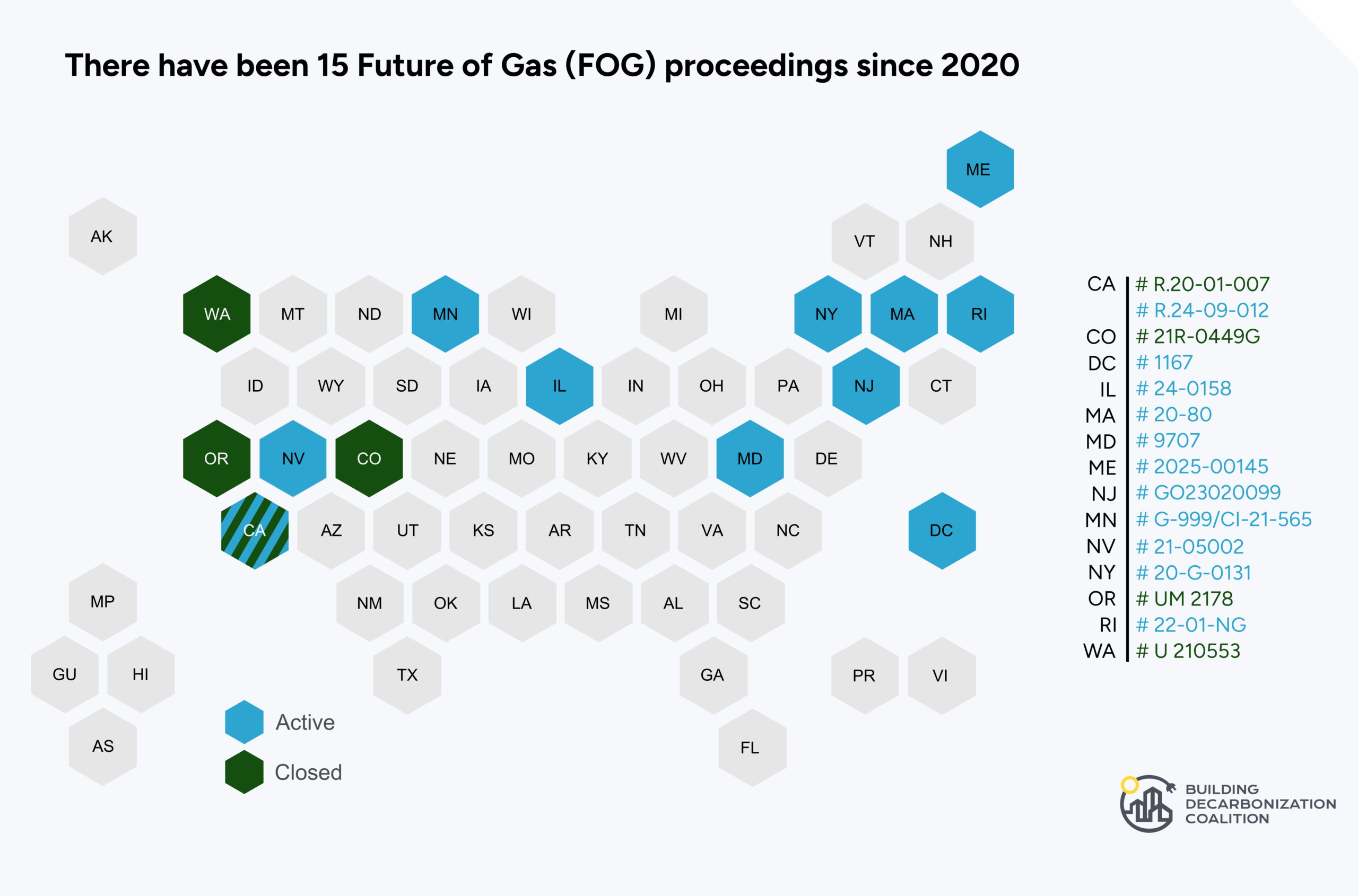

Future of Gas Proceedings

Since 2020, 15 proceedings that we consider to address the future of gas have been opened across 13 states and D.C. Currently, 11 proceedings are active, though not all have had recent activity. These proceedings have led to key insights on the inequitable distribution of methane pollution, the risks of business-as-usual gas system growth, and the urgency of reforming outdated policies. A managed, neighborhood-scale transition off the gas system requires clear decarbonization targets to halt expansion, limit reinvestment, and right-size the system.

For a comprehensive list of Future of Gas proceedings, including closed and inactive dockets, see BDC’s public tracker.

Figure 8: Summary of Future of Gas proceedings

Q2 Future of Gas Proceeding Highlights:

- California proposed an application process for neighborhood-scale decarbonization pilots. The CPUC’s proposed decision for SB 1221 would create three application rounds beginning December 15, 2026, assign pilot slots by utility, require utilities to show gas infrastructure can be decommissioned, and establish customer outreach, consent, cost-effectiveness, and behind-the-meter cost recovery requirements.

- Maine’s new Future of Gas docket sharpened the debate over how to evaluate future gas investments. Consumer and environmental advocates supported a stronger climate-and-ratepayer-risk screen, while gas utilities pushed for a more flexible framework that preserves safety, reliability, customer choice, and consideration of alternative fuels such as RNG.

- Maryland built a detailed evidentiary record for long-term gas planning reform. Phase II testimony from OPC, state agencies, PSC Staff, and environmental advocates focused on scenario-based forecasting, building electrification, declining gas demand, affordability, stranded-cost risk, non-pipeline alternatives, methane emissions, and stronger scrutiny of continued gas-system investment.

- Massachusetts gas utilities’ Climate Compliance Plans drew broad criticism from intervenors. DOER, the Attorney General, and environmental advocates argued that the plans do not satisfy the Department’s Future of Gas directives, while utilities defended the filings as the first step in an iterative planning process and resisted prescriptive requirements on NPAs, line-extension reforms, depreciation, stranded costs, and cost recovery.

- Minnesota made only limited changes to gas line extension allowances but added new reporting requirements. The PUC lowered CenterPoint’s footage allowance by twenty feet, left Xcel’s unchanged, and required utilities to report sustained reductions in gas throughput and survey customers, builders, and developers about what heating options they would choose without natural gas service.

|

State |

Recent Activity |

|

California Order Instituting Rulemaking to Establish Policies, Processes, and Rules to Ensure Safe and Reliable Gas Systems in California and Perform Long-Term Gas System Planning (R. 24-09-012) (Part 2, 2024-present under 24-09-012) (Part 1, 2020-2024 under R.20-01-007) |

The CPUC’s “Future of Gas Part 2” rulemaking (R.24-09-012) is intended to guide California’s long-term transition away from the gas system while advancing near-term decarbonization actions. The proceeding implements SB 1221 (2024), which authorizes up to 30 voluntary neighborhood-scale decarbonization pilots and modifies the gas “obligation to serve” by allowing utilities, with CPUC approval, to reduce the customer consent threshold to no less than 67%. The rulemaking is structured in phases addressing interim actions, long-term gas planning, and SB 1221 implementation, including required mapping of planned pipeline replacements and designation of priority decarbonization zones. In 2025, utilities submitted 10-year pipeline replacement maps and Priority Neighborhood Decarbonization Zones (PNZs) at the census tract level, prioritizing areas with demonstrated local support and a significant concentration of planned gas main replacements, and supplementing them with high-scoring environmental and social justice communities. The PNZ list remains subject to refinement, with the Commission expected to update and finalize the zones by the end of 2026. In Q1 2026, the Commission refined the issues for SB 1221 implementation, including how utilities must demonstrate community engagement, notice, property-owner consent, and cost recovery for behind-the-meter zero-emission alternatives. And in Q2 2026, the CPUC issued a proposed decision (PD) establishing the application process for SB 1221 pilots. The PD shifts the proceeding from general pilot design toward a structured application framework, with first-round applications due December 15, 2026. The Decision is expected to be voted on in July of 2026. Planned Pipeline Replacement Maps:

Q2 2026 Update SB 1221 Proposed Decision & Application Rounds

Pilot Eligibility, Customer Services, and Cost-Effectiveness

Customer Outreach, Consent, and Community Engagement

Behind-the-Meter Cost Recovery and Future Incentives

Comments on the PD were filed June 18th, 2026 with reply comments filed June 23, 2026. What’s Next

|

|

Illinois The Future of Natural Gas and issues associated with decarbonization of the gas distribution system (Docket # 24-0158) (2024-present) |

In March 2024, the ICC launched a statewide Future of Gas proceeding to examine how Illinois gas utilities’ infrastructure plans align with the state’s decarbonization and electrification goals. Following Phase 1 workshops in 2024, Phase 2 is now underway and organized into three subphases: Phase 2A on decarbonization pathways and technologies; Phase 2B on pilot development and decarbonization pathways working groups; and Phase 2C on legislative and regulatory options related to the future of gas. Q2 2026: Phase 2C: Summary of Initial Legislative and Regulatory Proposals

Decarbonization Pathways Study Status and Goals

What’s Next:

|

|

Maine Inquiry Regarding Future of Natural Gas (Case No. 2025-00145) (May 2025-present) |

The Maine Public Utilities Commission (MPUC) opened a new Future of Gas proceeding to examine how gas utility regulation should align with the State’s statutory greenhouse gas reduction goals (Notice of Inquiry). Maine law requires economy-wide emissions reductions of 45% by 2030 and 80% by 2050 (from 1990 levels), and carbon neutrality by 2045. The Commission is tasked with facilitating emission reductions consistent with these targets while ensuring safe, adequate, and reasonably priced service. The inquiry seeks to develop a framework to evaluate the climate impacts of gas infrastructure investments and supply commitments, assess alignment with state climate targets, and examine potential future pathways for methane gas. Initial scope comments (June 2025) revealed a clear split among stakeholders: gas utilities emphasized renewable natural gas (RNG) and hydrogen, while the Office of the Public Advocate, the Governor’s Energy Office, and labor and climate groups supported exploration of thermal energy networks (TENs) and other non-pipeline alternatives. After a January 2026 workshop where E3 reviewed other states’ Future of Gas frameworks and the Office of the Public Advocate presented a matrix-based evaluation tool, the Commission’s February 2026 procedural orders moved the docket into a written-comment phase. Q2 2026: Comments Responding to Procedural Order

What’s Next

|

|

Maryland Case No. 9707

|

In February 2023, Maryland’s Office of People’s Counsel (OPC) petitioned the Public Service Commission (PSC) to open a Future of Gas proceeding to evaluate whether gas utility planning, practices, and rates remain “just and reasonable” and consistent with the public interest (pg. 7). Following public comments in 2024 and a renewed OPC petition in 2025, the PSC issued an order on June 13, 2025 signaling its intent to eliminate gas line extension allowances (LEAs) for new connections. The PSC reasoned that subsidies encouraging gas system expansion may conflict with Maryland’s climate goals and obscure the true cost of gas service. Staff were directed to propose LEA regulations by December 1, 2025, to be addressed through Rulemaking 92. On August 20, 2025, the PSC formally opened a comprehensive Future of Gas proceeding (Order 91791) within Case No. 9707 to examine the long-term role of natural gas in light of Maryland’s greenhouse gas reduction and electrification commitments. Citing the Climate Solutions Now Act and the Next Generation Energy Act, the Commission will evaluate:

Q2 2026: Phase II Testimony Record

LEA Reform (RM 92)

What’s Next:

|

|

Massachusetts The Future of Gas (Docket #: 20-80) (2020-present) Utility Climate Compliance Plans: (25-40, 25-41, 25-42, 25-43, 25-44, 25-45) |

In its landmark December 2023 order in the “Future of Gas” docket, the Massachusetts Department of Public Utilities (DPU) established a new standard for gas system investment consistent with the state’s net-zero by 2050 mandate. The DPU shifted the burden of proof to gas utilities, requiring them to demonstrate that non-pipeline alternatives (NPAs) are either not cost-effective or infeasible before proceeding with major gas infrastructure investments, including full pipeline replacements. This marked a departure from business-as-usual gas expansion and laid the groundwork for reassessing long-term stranded asset risk and ratepayer exposure. In 2024, the DPU turned to reforming gas line extension allowances (LEAs). Utilities were directed to report on their LEA practices, and in a February 5, 2025 memorandum, the Department proposed eliminating LEAs by requiring new customers to pay the full cost of connecting to the gas distribution system. The proposal further stated that “no costs associated with a new service or line extension shall be deemed prudently incurred and, thus, eligible for inclusion in an LDC’s rate base” (Feb. 5, 2025 Memorandum). Implementation is occurring through the 2025 Climate Compliance Plan (CCP) dockets: D.P.U. 25-40 for Berkshire Gas, D.P.U. 25-41 for National Grid, D.P.U. 25-42 for Unitil, D.P.U. 25-43 for Liberty, and D.P.U. 25-44/25-45 for Eversource’s EGMA and NSTAR Gas companies. These dockets are the mechanism for implementing D.P.U. 20-80-B‘s requirements on emissions-reduction planning, NPAs, line-extension policy, decommissioning, and stranded-cost risk. The initial CCP were filed in April 2025 and were supposed to expand on the utilities’ net-zero enablement plans, detail total investment necessary and at least one alternative pathway, include customer/stakeholder/community input, and report on hybrid-heating switchover practices. The CCP dockets are also the forum for investigating NPA analysis before pipeline projects, decommissioning and depreciation practices, stranded costs from GSEP investments, whether GSEP should be combined into CCP review, and line-extension allowance policies. In a subsequent Interlocutory Order, the DPU proposed a simplified policy to eliminate LEAs and clarified that final determinations would be made within these CCP dockets. Utilities sought a stay, citing procedural concerns, but the Department directed them to file revised tariffs reflecting removal of LEAs. At the same time, the Department began evaluating how the state’s 2024 climate law (S. 2967) reshapes the gas “obligation to serve,” including whether utilities may retire gas service in favor of electrification or thermal energy networks, and whether neighborhood-scale decarbonization projects can proceed without unanimous customer consent. The central question is whether the obligation to serve guarantees indefinite gas service upon request, or whether the DPU may permit targeted retirement of gas infrastructure where adequate non-gas alternatives exist. This issue is critical to whether neighborhood-scale electrification or thermal energy network projects can proceed without unanimous customer consent. From April to June 2026, utilities and intervenors filed initial and reply briefs regarding the utilities’ CCPs. The most significant development was broad criticism of the CCPs from DOER, the Attorney General, and environmental/consumer advocates, who argues that the utilities’ plans do not comply with the Department’s Future of Gas directives and are simply enabling the continuance of a business-as-usual gas expansion framework. Q2 2026: April 2026 Initial Briefs Challenging the Plans

Utility Response

What’s Next:

|

|

Minnesota In the Matter of a Commission Evaluation of Changes to the Natural Gas Utility Regulatory and Policy Structures to Meet State Greenhouse Gas Reduction Goals (Docket #: G-999/CI-21-565) (2021-present) |

In 2021, the Minnesota Legislature directed the Public Utilities Commission (PUC) to evaluate changes to natural gas regulatory structures needed to meet or exceed the state’s greenhouse gas reduction goals. The Commission opened the Future of Gas docket (G999/21-565) to implement this directive. Much of the early work proceeded through gas utilities’ Integrated Resource Plan (IRP) proceedings, culminating in March and October 2024 orders addressing modeling assumptions, emissions pathways, and planning transparency. In January 2025, the Commission reset the scope and timeline, returning focus to the Future of Gas docket. Current informational hearing topics include winter reliability, renewable natural gas (RNG), hydrogen and other alternative fuels, hybrid heating rate design, and updates from the Thermal Energy Network (TEN) Work Group. In parallel, the Commission initiated review of gas line extension allowance (LEA) policies before a comment period evaluating changes to rates to promote heat pump affordability and evaluate and address stranded asset risks as a result of electrification. In June 2026, the Commission met to discuss the LEA policy, among other issues, and determined that they would only make minor modifications to the policy (see the LEA summary above). Q2 2026: June 4th Hearing

What’s Next

|

|

New York Proceeding on Motion of the Commission in Regard to Gas Planning Procedures (2020-present)

|

The New York gas planning docket (20-G-0131) originated in response to gas moratoria concerns but has since identified the need for a statewide framework for managed gas transition planning. The PSC now requires each gas utility to file a Long-Term Gas Plan (LTGP) every three years in separate utility-specific dockets. Each LTGP must include at least one scenario with no new traditional gas infrastructure, quantify greenhouse gas impacts, evaluate non-pipeline alternatives (NPAs), and provide updates on demand forecasts, electrification progress, and system risks. Q2 2026:

Utility-Specific Gas Planning: Central Hudson Gas & Electric (23-G-0676):

New York State Electric & Gas Corporation and Rochester Gas and Electric (23-G-0437):

ConEd and Orange and Rockland Utilities (23-G-0147):

National Grid (24-G-0248):

National Fuel Gas Distribution Corp. (22-G-0610):

What’s Next (Long-Term Gas Plans)

|

|

Rhode Island Investigation into the Future of the Regulated Gas Distribution Business in Rhode Island |

The Rhode Island Public Utilities Commission opened the Future of Gas investigation in June 2022 to examine the future of the regulated gas distribution business in light of the Act on Climate. The docket produced extensive stakeholder process work and an E3 technical analysis, but has not had significant activity in the past year. The most meaningful development in 2026 is how the Future of Gas issue of gas line extension allowances surfaced in RI Energy’s pending 25-45-GE electric/gas rate case and in companion House (H7891) and Senate (S2354) resolutions that are asking the PUC to terminate gas line-extension allowances in that rate case. Q2 2026:

|

Future of Heat Regulation

Q2 Highlights:

- California utilities laid out different visions for energy efficiency and electrification. In their 2025 Energy Efficiency annual reports, PG&E emphasized building electrification, financing, load flexibility, and neighborhood-scale pilots; SCE framed efficiency as a grid and affordability resource; SDG&E argued for a smaller, more targeted portfolio; and SoCalGas defended a fuel-neutral approach that continues to support high-efficiency gas measures.